Operating by Warren & Charlie

The Operating by John Brewton Black Friday Post: Dissecting Warren Buffett & Charlie Munger's approach to operating as described by four of their seminal deals

Check out these reader favorites:

Buffett and Munger did not build Berkshire by “finding cheap stocks.”

They built it by marrying capital to operators who could run exceptional businesses for decades with almost no interference.

That is the real meaning of “our favorite holding period is forever.”

How Berkshire Actually Used “Forever”

When Buffett talks about forever, he is referring to a specific structure: find a business with durable economics, pair it with an exceptional manager, and then give them the time, autonomy, and capital they need. The compounding comes from the operator–business pairing, not from clever trading.

This philosophy is codified in Berkshire’s Owner’s Manual, a document Buffett first wrote in 1996 and has updated periodically since. The manual lays out 15 principles, but the core thesis is simple: Berkshire is a collection of businesses run by autonomous operators who think like owners, supported by a parent company that provides capital and stays out of their way.

The practical application of this philosophy shows up in Berkshire’s Acquisition Criteria, which has remained largely unchanged for decades. The criteria explicitly state: “We need management in place (we can’t supply it).” Berkshire does not buy turnarounds. It does not install heroic new CEOs. It buys businesses where the operator is already exceptional and wants to keep running the company.

Four acquisitions show the pattern clearly: See’s Candies, GEICO, Nebraska Furniture Mart and BNSF Railroad. In each case, the long holding period was earned by management behavior and operating results, not granted in advance as a virtue signal.

Compounding on a Small Base

Berkshire bought See’s in 1972 for approximately $25 million, when it was generating roughly $4 million in pretax profit on about $8 million of tangible capital. That looked expensive on traditional value screens. What changed Buffett’s mind was the realization that See’s had genuine pricing power: customers would accept price increases well above inflation without switching because the product and brand were embedded in habit and emotion.

The key to the acquisition was Chuck Huggins, a 20-year See’s veteran who became president. In a 1972 letter to Huggins that has since become legendary among Berkshire students, Buffett laid out his operating philosophy in plain language.

The instructions were remarkably simple: never sacrifice quality for profit, keep production local, protect the brand’s reputation. No growth hacks. No rapid scaling. No pressure to hit quarterly targets. Just protect the moat and let pricing power compound.

Buffett’s letter included a revealing comparison to Coors beer: “I always had the suspicion that 99% was in the telling and 1% was in the drinking.” This was a remarkably honest admission that brand storytelling—not just product quality—creates pricing power. Huggins understood this intuitively and spent the next three decades protecting See’s positioning while methodically raising prices.

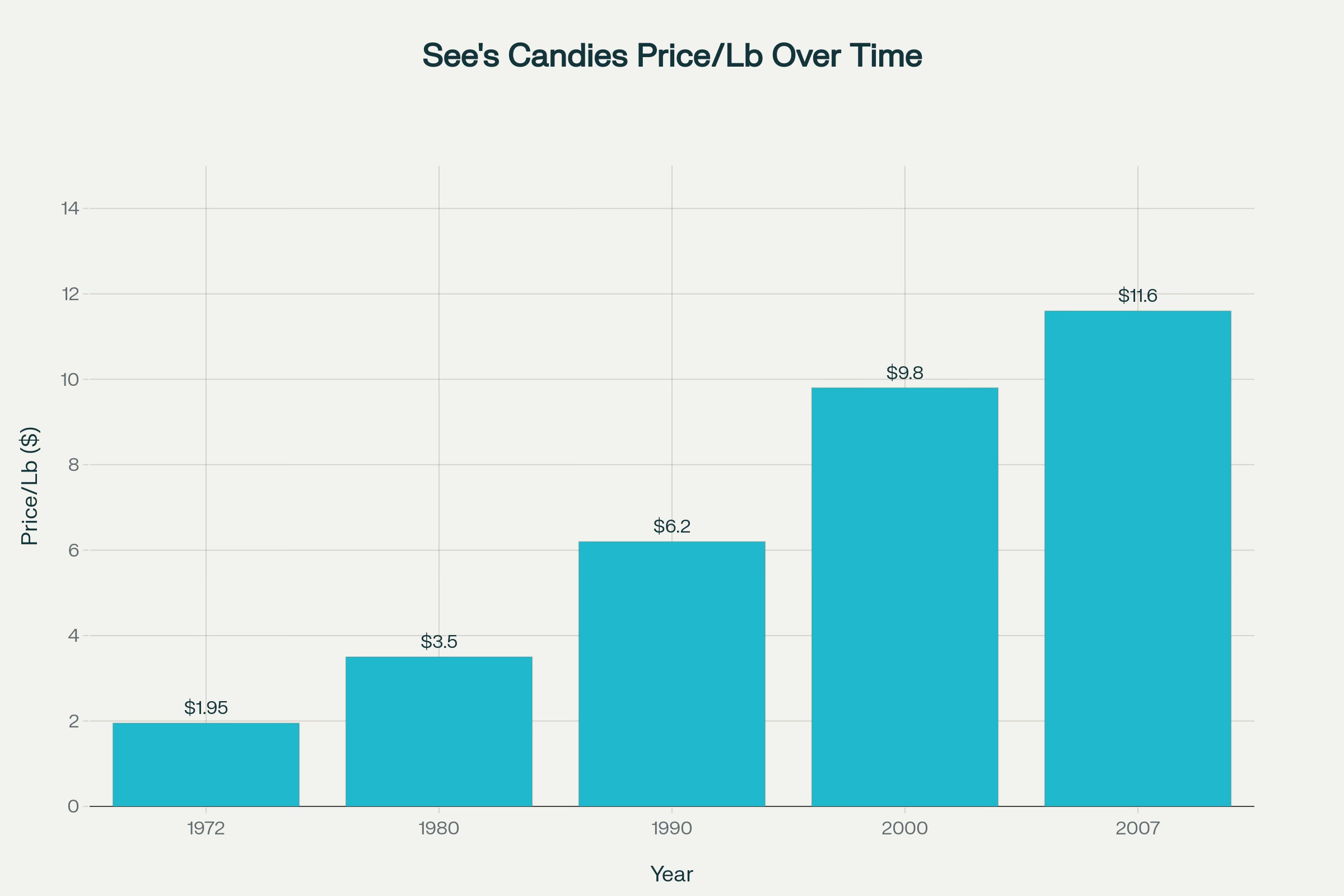

The results over 35 years:

$25 million invested → $2 billion+ in cumulative pretax earnings sent to Berkshire

Only $32 million of additional capital reinvested

Price per pound: $1.95 → $11.60+ (roughly 7-8% annual increases, far above inflation)

Revenue: $30 million → $430 million

Effective returns: 8,000%+ on original investment

“See’s gave birth to multiple new streams of cash for us,” Buffett later wrote. The cash from See’s funded acquisitions of other businesses, which generated more cash, funded more acquisitions. The compounding was not just within See’s—it was across Berkshire’s entire portfolio.

What made it work was not a turnaround or a brilliant strategic pivot. It was a disciplined exploitation of an existing moat by an operator who understood the business deeply and had no desire to “grow” it into mediocrity. Volume grew about 4% annually. Prices grew at about an 11% annual rate, representing slow growth but fast compounding.

Huggins ran See’s until 2005, over three decades of continuous operation under the same philosophy. Buffett called See’s his “prototype of a dream business” and credited it with teaching him that paying up for quality, when paired with exceptional management—was superior to buying mediocre businesses at a low price.

Berkshire completed its purchase of GEICO in 1995, paying approximately $2.3 billion for the half of the company it did not already own. At that point, GEICO had a small, single-digit share of the U.S. auto market but a clear structural edge: a direct-to-consumer, low-cost model that allowed it to spend more on marketing while still underpricing many of its competitors.

GEICO: Scaling a Cost Advantage

Berkshire’s relationship with GEICO began in 1951 when Buffett, then a 20-year-old Columbia student, visited the company’s headquarters on a Saturday and spent four hours learning about the business from Lorimer Davidson. Buffett invested a significant portion of his net worth and later sold for a profit, but GEICO stayed lodged in his memory as an example of structural competitive advantage.

In 1976, GEICO nearly went bankrupt. Buffett began repurchasing shares, eventually accumulating a 50% stake by 1980. In 1995, Berkshire paid $2.3 billion to acquire the remaining 49% it did not already own.

At that point, GEICO was the seventh-largest auto insurer in the United States with roughly 2.5% market share. The business had a clear structural advantage: a direct-to-consumer model that eliminated agent commissions, allowing it to undercut competitors on price while still earning underwriting profits.

The operator who would scale this advantage was Tony Nicely, who became CEO in 1993. Nicely had joined GEICO in 1961 as a 19-year-old and worked his way up through the company over the course of three decades. He understood the cost structure intimately and had a clear thesis: GEICO’s advantage would compound with scale, because fixed costs could be spread across more policies. At the same time, the direct model kept variable costs low.

The key passage from Buffett’s 1995 Shareholder Letter explained the strategic logic: “In business, I look for economic castles protected by unbreachable moats.” GEICO’s moat was its cost structure. Nicely’s job was to widen it.

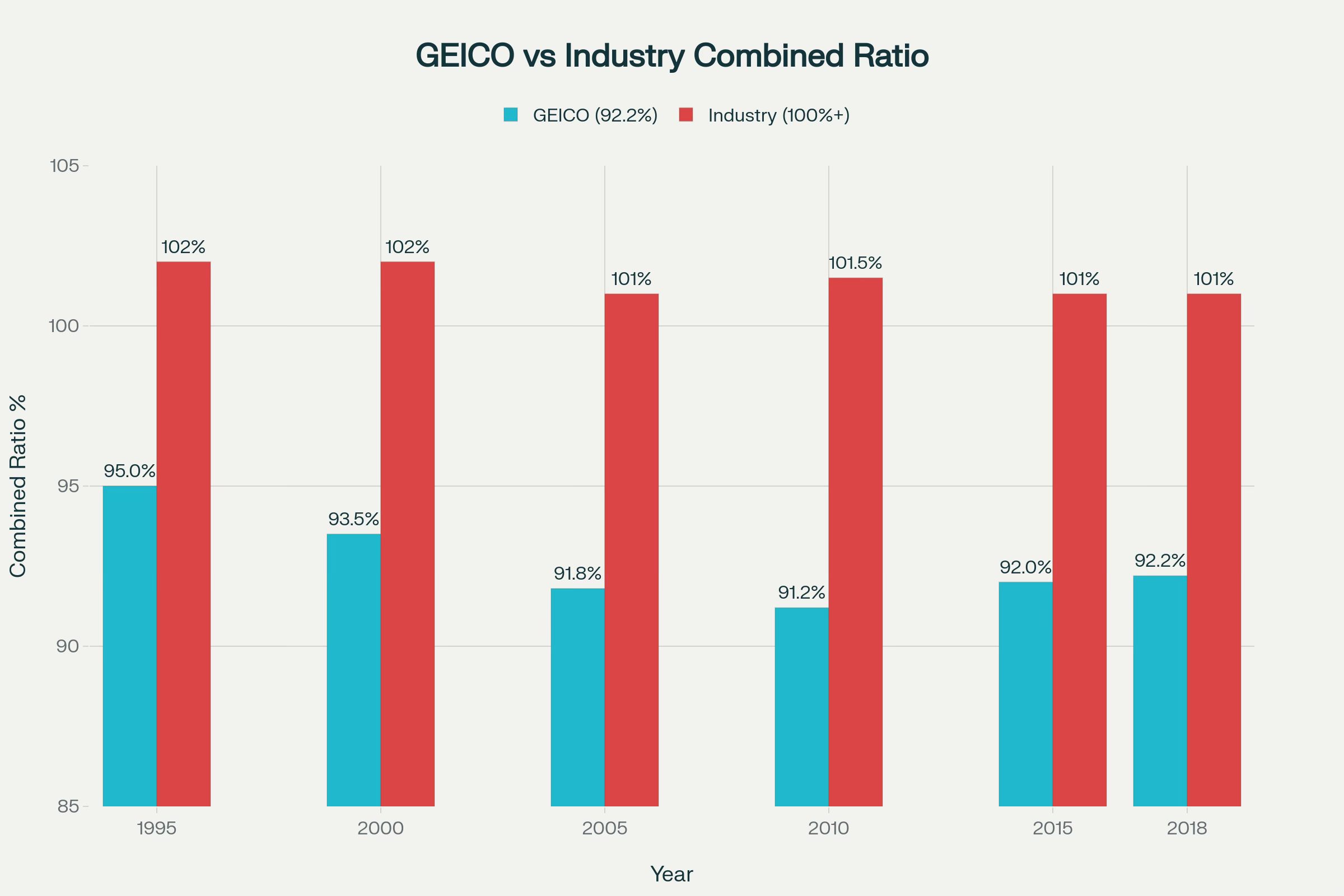

The results over Tony Nicely’s 25-year tenure:

Market share: 2.5% → 14%+ (now second-largest auto insurer in U.S.)

Policies: ~2 million → 18 million+

Premiums earned: grew at 9.1% compound annual rate

Combined ratio: 92.2% average (vs. 100%+ industry average)

Cumulative underwriting profit: $9.7 billion+

Float: $3 billion → $12.5 billion+

The combined ratio is the key operating metric. A combined ratio below 100% means the company is earning an underwriting profit; it collects more in premiums than it pays out in claims and expenses. Most auto insurers hover around 100% or above, meaning they break even on underwriting and make money by investing the float. GEICO consistently earned underwriting profits, allowing it to invest the float.

Buffett’s 2018 assessment of Nicely’s tenure was unequivocal: “Tony’s management of GEICO has increased Berkshire’s intrinsic value by more than $50 billion.”

The operating edge came from relentless focus on the direct model. GEICO’s expense ratio remained around 18%, while the industry average was 25%. That 7-point advantage funded both aggressive advertising (GEICO spent over $1 billion annually on marketing by the 2010s) and lower prices for customers. Scale begat more scale.

Nicely retired in 2018 after 57 years at the company. Competitors have since copied the direct-to-consumer model he scaled, but GEICO’s head start and accumulated brand awareness have proven difficult to replicate.

The Handshake Deal

In 1983, Buffett bought 90% of Nebraska Furniture Mart for $60 million. The acquisition contract was 1.25 pages long.

There was no audit. No verification of receivables. No inventory check. Buffett did not even visit the store before making the offer. He trusted the word of the 89-year-old woman who ran it.

Rose Blumkin—”Mrs. B”—had emigrated from Russia in 1917, speaking no English. She started Nebraska Furniture Mart in 1937 with $500 in savings and built it into the largest furniture store in North America by following a simple formula: buy in bulk, operate on thin margins, never lie to customers.

Her credo, repeated constantly to employees and customers alike: “Sell cheap, tell the truth, don’t cheat nobody.”

Buffett’s 1983 Shareholder Letter devoted considerable space to explaining why he paid a premium for NFM without conducting due diligence. The answer was Mrs. B herself. Buffett had watched her operate for years, seen her competitive behavior up close (she had repeatedly beaten competitors who tried to undercut her), and concluded that her character was the due diligence.

“Mrs. B simply told me what was what, and her word was good enough for me,” Buffett wrote.

The economics of NFM were driven by purchasing power and fixed-cost leverage. The Omaha store did more volume than any furniture retailer in the country, which meant suppliers gave preferential pricing. The high volume also meant fixed costs (rent, management, systems) were spread across more revenue. Competitors with smaller stores could not match NFM’s prices without losing money.

The results over four decades:

Original 90% stake: $60 million

Current structure: stores in Omaha, Kansas City, and Dallas/Fort Worth

Omaha and Kansas City stores: each does roughly $450 million in annual revenue

Dallas store: did $500 million+ in its first partial year (opened 2015)

Total estimated revenue: $1.2-1.6 billion annually

Still family-managed under the Blumkin family

Mrs. B kept working 12-14 hours a day, seven days a week, until she was 103 years old. She briefly “retired” at 95 and opened a competing store across the street from NFM, forcing Berkshire to buy her out a second time. Her relentlessness was both the source of NFM’s competitive advantage and the reason Buffett wanted to own it.

The lesson from Nebraska Furniture Mart is that management assessment is not primarily about analyzing org charts or incentive structures. It is about character. If you need extensive due diligence to trust the operator, you are probably buying the wrong business.

Patient Capital in Heavy Industry

Berkshire’s 2010 acquisition of BNSF Railway looked like the opposite of See’s Candies: asset-heavy, cyclical, capital-intensive, and heavily regulated. The price—approximately $44 billion including debt—was Berkshire’s largest acquisition ever.

The attraction was not a quick efficiency fix. It was the chance to own a strategic infrastructure asset run by a management team already executing well and willing to reinvest at scale.

Buffett called it “an all-in wager on the economic future of the United States.” Railroads move coal, grain, consumer goods, and intermodal containers more efficiently than trucks over long distances. If the U.S. economy grows, rail volumes grow. If fuel costs rise, rail’s efficiency advantage over trucking increases.

Matt Rose, who had been CEO since 2000, stayed on after the acquisition. In a 2015 interview, Rose described the relationship with Buffett: “Warren is my boss, and it’s a happy marriage. He lets us run the railroad.”

The Berkshire ownership model for BNSF has been consistent: provide patient capital for long-payback infrastructure investments that public market investors might pressure management to defer. Since the acquisition, BNSF has invested approximately $3-4 billion annually in track, rolling stock, and capacity upgrades.

From Berkshire’s 2009 Shareholder Letter, written just after announcing the deal: “Our country’s future prosperity depends on its having an efficient and well-maintained rail system... Berkshire is making a large and long-term commitment to BNSF.”

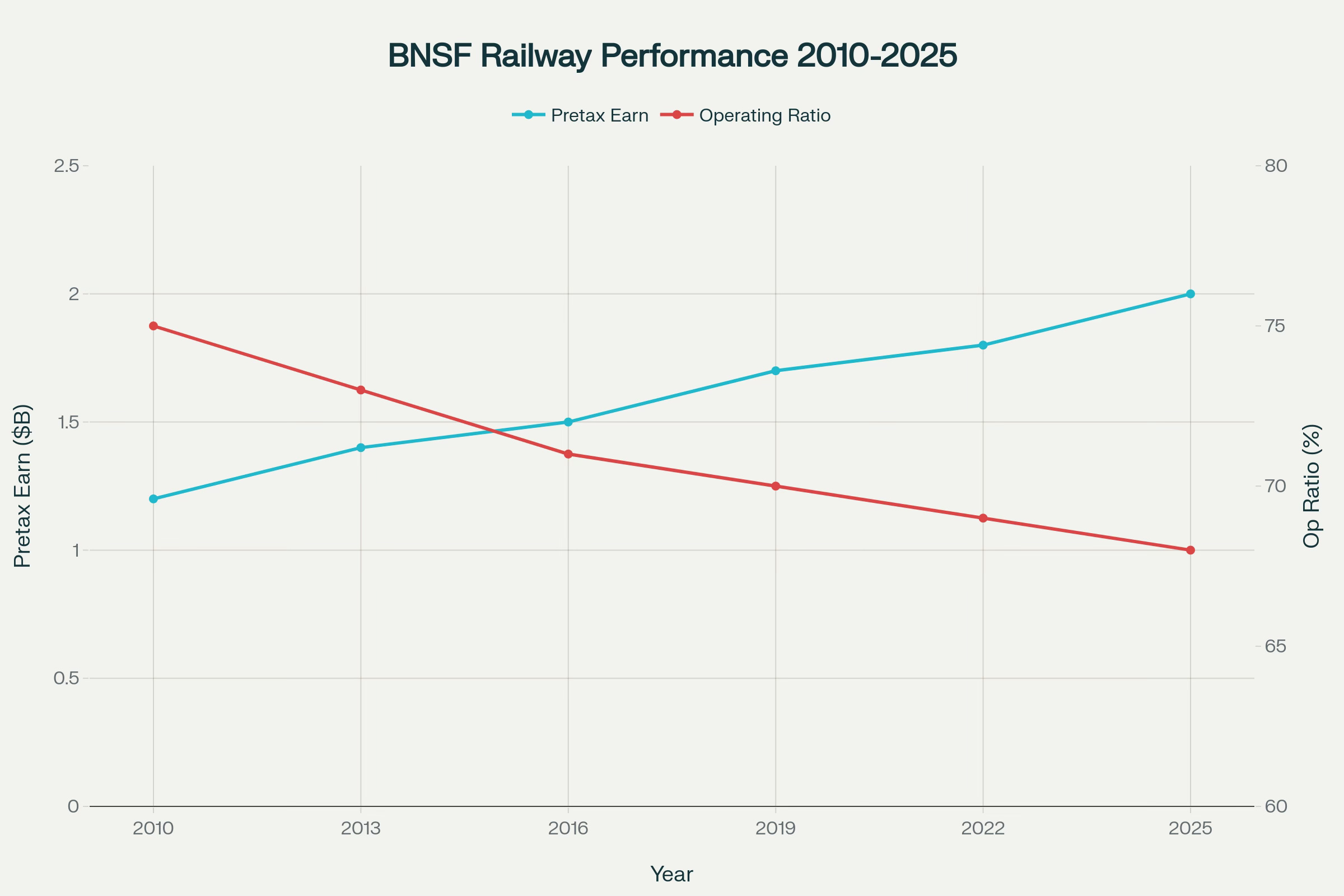

The results over 15 years:

Annual capital investment: $3.8 billion planned for 2025 alone

Expansion investment over past 5 years: $2.6 billion+

Q2 2025 pretax earnings: $2 billion (up 11.5% year-over-year)

Cumulative operating cash since acquisition: $90 billion+

Current estimated value: significantly above original purchase price

The “improvement” at BNSF is less about fixing a broken operator and more about combining a capable management team with an owner willing to fund investments others might avoid. Public market railroads face pressure to return capital to shareholders. BNSF, under Berkshire, can prioritize network capacity and service quality over quarterly earnings.

Rose retired in 2020 after two decades as CEO, having led BNSF through its transition from public company to Berkshire subsidiary. The operating philosophy remained unchanged: invest in the network, maintain service quality, think in decades rather than quarters.

The “improvement” here is less about fixing a broken operator and more about combining a capable management team with an owner willing to fund long-term, high-return investments that others might avoid.

The Pattern: What All Four Share

The “Forever” Holding Period: Four Acquisitions, 15-53 Years of Patient Capital

Across candy, insurance, furniture retail, and railroads, Buffett and Munger did the same thing:

Insisted on proven management before buying. Berkshire’s acquisition criteria explicitly state: “We need management in place (we can’t supply it).” In every case—Huggins at See’s, Nicely at GEICO, Mrs. B at NFM, Rose at BNSF—the operator was already running the business successfully before Berkshire arrived. There were no turnaround projects, no imported executives, no 100-day plans.

Selected for character, not just competence. The 1.25-page NFM contract and the absence of due diligence illustrate the point: if you trust the operator’s character, you do not need elaborate protections. If you do not trust their character, no contract will save you.

Delegated almost completely. Buffett’s description of his management style: “We delegate almost to the point of abdication.” The only things subsidiary managers must clear with Omaha: changes to post-retirement benefits, significant acquisitions, and unusually large capital expenditures. Everything else is autonomous.

Protected reputation above profits. Every two years for more than 25 years, Buffett sent a one-page memo to all Berkshire managers with the same message: “The top priority—trumping everything else, including profits—is that all of us continue to zealously guard Berkshire’s reputation. We can afford to lose money—even a lot of money. But we can’t afford to lose reputation—even a shred of reputation.”

Held for decades. See’s has been owned for 53 years. GEICO for 30 years since full acquisition (49 years since Buffett resumed buying). Nebraska Furniture Mart for 42 years. BNSF for 15 years and counting. “Forever” is not a slogan; it is a consequence of finding combinations of business model, market position, and management where time strengthens the economics instead of eroding them.

What This Means for Operators

The Berkshire model is not primarily an investment framework. It is an operating framework. The lesson is not “buy and hold good stocks.” The lesson is that exceptional long-term outcomes come from:

Businesses with durable competitive advantages (moats)

Operators with integrity, competence, and owner mentality

Organizational structures that give operators autonomy

Capital allocation that prioritizes reinvestment over extraction

Time horizons measured in decades, not quarters

Most modern “operating advice” diverges sharply from this. The internet is flooded with systems for exponential growth, funnels and playbooks, and obsession with top-line metrics at all costs.

Buffett and Munger focused on the craft of managing an enduring enterprise. That is the same target for Operating by John Brewton: not “how to jack MRR next month,” but how real companies have actually been operated—strategy, incentives, capital allocation, and organizational design—and what that implies for becoming a better operator and capital allocator today.

“Forever” is not a slogan; it is a consequence of finding combinations of business model, market position, and management where time strengthens the economics instead of eroding them.

- john -

Appendix: Primary Sources and Further Reading

If you want to read Buffett and Munger in their own words on these acquisitions and management principles, here is a curated library of the documents that matter most.

The Letters That Shaped Berkshire’s Operating Philosophy

See’s Candies

1972 Letter to Chuck Huggins — Buffett’s original instructions on protecting the See’s brand and culture

2007 Shareholder Letter — Detailed retrospective on See’s pricing power and returns after 35 years

Nebraska Furniture Mart

1983 Shareholder Letter — The acquisition announcement and Buffett’s explanation of why he trusted Mrs. B

NFM Offer Letter and 1946 Financials — The legendary 1.25-page handshake deal

GEICO

1995 Shareholder Letter — Full acquisition rationale and Tony Nicely assessment

BNSF Railway

2009 Shareholder Letter — Acquisition announcement and “all-in wager on the American economy” thesis

Latest Thinking

2024 Shareholder Letter — Most recent letter reflecting on 60 years of compounding

Foundational Documents

How Berkshire Operates

Owner’s Manual — Buffett’s 15 principles for how Berkshire operates and treats shareholders

Acquisition Criteria — The official (and remarkably brief) criteria for what Berkshire looks for in businesses

Management Philosophy

Biennial Memo to Managers — The “reputation over profits” memo Buffett sent every two years for 25+ years

Complete Archive

All Shareholder Letters (1965-2024) — 60 years of unfiltered thinking from Buffett

Secondary Sources Worth Reading

See’s Candies

Financial Teardown of See’s Candies — Detailed quantitative analysis of See’s returns and economics

GEICO

GEICO In Numbers — Historical data on GEICO’s growth under Berkshire ownership

Nebraska Furniture Mart

Rose Blumkin Biography — Deep profile of Mrs. B’s life and operating philosophy

BNSF Railway

Revisiting the BNSF Acquisition — Analysis of the deal three years after closing

Matt Rose on Working for Buffett — BNSF CEO describes the Berkshire relationship

I hope you enjoy reading these as much as I have.

- j -

Uncle Charlie and uncle Warren will continue to inspire for generations

Really enjoyed this! especially how clearly you show that the real edge wasn’t brilliance in deals, but patience in structure.. You make a subtle point that often gets missed: durable systems come from disciplined alignment, not constant optimization.

Discipline is sadly a rarity these days, even though it is discipline that is the mother of victories..