We Are All Becoming Operators

The Historical and Technological Evolution of the Company

Three forces are converging.

Technology lowers the floor on what one person can produce.

Capital restructures around small teams and individual operators.

History will reward the first-movers.

The combination is turning workers into operators of their own enterprise.

The shift from traditional employment to micro-entrepreneurship is the culmination of centuries of economic evolution. Digital platforms and AI carry the cost curve the rest of the way down. “Company” no longer requires size or hierarchy. It now signals autonomous agency in a global market. This article traces the historical arc, examines why the tools now exist for any individual to operate as a company of one, and anticipates a future in which large companies behave as cellular networks of human-centered micro-organizations.

Current outcomes are unevenly distributed. Embedded risks are plentiful. The history is still being lived. The pattern is clear enough to act on. A large share of global working economic activity will function this way within the decade.

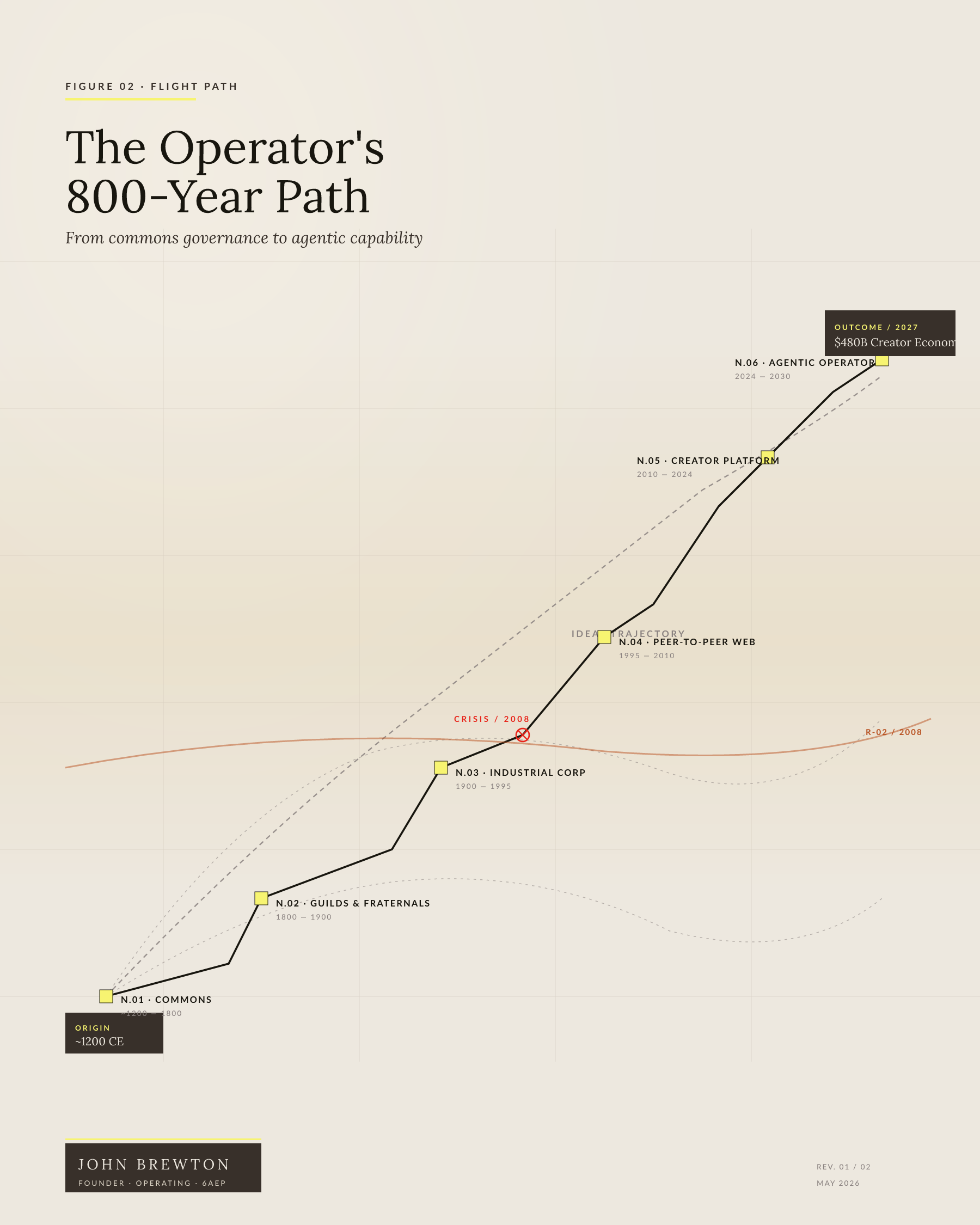

From Commons to Corporations

Pre-industrial systems built the bedrock for shared economic activity. Medieval villages managed farmland, pasture, and forest as commons, governed by rules ensuring equitable access. Elinor Ostrom’s Nobel-winning research documented more than 800 such common-pool resource arrangements across centuries and continents. Her 1990 book Governing the Commons showed that local users repeatedly designed governance frameworks that avoided the tragedy of the commons. The same ethos resurfaced in 19th-century mutual aid societies. David T. Beito’s research documents how fraternal and friendly societies provided sickness benefits, burial benefits, orphanages, and health care systems to a broad cross-section of Americans before the welfare state. At the peak, more Americans belonged to fraternal societies than to any other voluntary association except churches.

Industrialization reorganized economic life. Mechanized factories replaced artisanal production. Corporations emerged as centralized entities optimized for scale and efficiency. Franchise models like Ford’s assembly line standardized operations. Precursors to today’s platforms already existed during this period. Nineteenth-century grain exchanges functioned as physical matchmaking platforms, connecting buyers and sellers through trusted intermediaries.

The digital revolution’s first wave transformed peer-to-peer exchange. eBay launched in 1995 as a side project by Pierre Omidyar, digitizing flea markets and classified ads. Craigslist expanded the model into services and housing. Both platforms introduced reputation systems, digital proxies for community trust. The peer-review reputation mechanism reduced transaction friction and became the blueprint for Amazon Marketplace, Airbnb, Uber, Etsy, and Fiverr. The NBER’s peer-to-peer markets research by Einav and Farronato shows how each generation of platform pushed the trust signal further out into a stranger-to-stranger commerce model. Amazon then converted Walmart’s physical retail concept into an online operating system at planetary scale.

Platform Entrepreneurship

The 2008 financial crisis triggered a structural shift in the labor market. As unemployment climbed, online labor platforms absorbed displaced workers. The Resolution Foundation's analysis of UK labor market data found that self-employment accounted for 45 percent of all UK employment growth after March 2008. Self-employment grew by 650,000 from 2008 to a peak of 4.5 million, nearly 15 percent of UK employment. Two-thirds of UK post-crisis job creation came from atypical roles: self-employment, zero-hours contracts, and agency work.

In the United States, Katz and Krueger’s Princeton-RAND research tracked the share of workers in alternative arrangements (temp, on-call, contract, independent) climbing from 10.7 percent in February 2005 to 15.8 percent in late 2015. Contract company workers more than doubled in that window. Uber, Airbnb, and TaskRabbit were founded in this period. They used underutilized assets (cars, homes, labor) and grew precisely because traditional systems faltered.

The period normalized three trends:

Fragmentation of work from stable employment to project-based engagements

Rise of micro-enterprises absorbing a meaningful share of new job creation

Digital-first business models that priced access above ownership

Hall and Krueger’s 2018 ILR Review analysis of Uber’s driver-partners found that most drivers held full- or part-time employment before joining the platform and continued in those roles after. Platforms were not replacing jobs in this period. They were supplementing income and giving workers a flexible income fallback.

Figure 02. The Operator’s 800-Year Path. From commons governance to agentic capability.

COVID-19: The Greatest Accelerator

The COVID-19 pandemic pulled forward a decade of change in two years. Barrero, Bloom, and Davis’s Stanford-Hoover research tracked U.S. full work-from-home shares from roughly 5 percent before the pandemic to nearly 60 percent in spring 2020, then settling near 28 percent by 2023. Their American Economic Association paper on the evolution of remote work confirms a roughly four- to fivefold increase over baseline that has persisted for three years past the trigger event.

MIT Sloan Management Review documented productivity gains across 90 percent of firms in the first year of remote work, with 55 percent of home-based workers reporting higher output. Lynda Gratton’s seven-truths analysis found that teams together 23 to 40 percent of the time performed best across multiple performance dimensions.

The shift democratized access to global talent pools. Companies hired across borders. Workers competed and collaborated across borders. The result is what Stanford GSB now describes as a borderless professional services market.

The entrepreneurial response was structural. McKinsey’s American Opportunity Survey found that 36 percent of employed Americans, roughly 58 million people, identified as independent workers in 2022. That share is up from 27 percent in 2016. Of those, 76 percent identified as contract, freelance, or temporary workers, and 68 percent identified as gig workers.

The U.S. Census Bureau’s non-employer business data show the same pattern from a different angle. Non-employer businesses grew at 4.9 percent in 2021 and 4.7 percent in 2022, the fastest rates in nearly two decades. The United States now contains roughly 29.8 million solopreneurs producing about $1.7 trillion in annual revenue.

Outcomes remained uneven. Workers with digital skills and access to platforms captured the upside. Workers without were exposed to downward pressure on earnings and persistent precarity.

The Creator Economy: Vanguard of the Operator Revolution

Beyond Influencers to Economic Transformation

The creator economy has been treated as synonymous with social media influencers. That framing misses the larger pattern. The infrastructure that produced the influencer (audience-building tools, direct monetization, AI-powered content creation, global payment processing) is now adopted by a far broader population. Andreessen Horowitz called this the passion economy in Li Jin’s 2019 framing. The thesis was that new platforms allow anyone to monetize unique skills, in contrast to earlier marketplaces that flattened individuality and commoditized labor.

The current infrastructure becomes the operational backbone for:

Professional services (consulting, coaching, specialized expertise)

Digital craftsmanship (design, development, custom solutions)

Knowledge work (research, analysis, education)

Hybrid enterprises that combine content, products, and services

Projected Economic Significance

Goldman Sachs Research estimates the global creator economy at $250 billion today, growing to $480 billion by 2027 at a roughly 14 percent compound annual growth rate. The global creator base of 50 million is projected to grow 10 to 20 percent annually for the next five years.

Income concentration remains a problem. Only about 4 percent of global creators earn more than $100,000 per year. Li Jin’s HBR essay argues for platform mechanisms that build a creator middle class, not just more lottery winners at the top. The fix is structural. Discovery algorithms, revenue-sharing terms, and audience portability determine who builds a stable business and who does not.

By 2027, more than half of U.S. households will derive some portion of household income through creator economy channels and platforms. The creator economy stops being a side-hustle phenomenon and becomes a core piece of household income, community formation, and operating models inside traditional corporations.

V. Modern Infrastructure: The Platform Stack

Today’s operator economy rests on three layers of infrastructure. Each solves a constraint that historically required scale.

1. Social Networks as Marketplaces

LinkedIn and TikTok democratized audience-building and distribution. What once required a corporate marketing budget is now achievable through organic content. Individuals become media entities. Instagram storefronts and TikTok creator funds enable direct monetization. The boundary between creator and entrepreneur dissolves.

2. AI as the Operational Backbone

Tools like ChatGPT and Claude automate work that historically required specialized departments:

Content creation (replacing copywriters and junior marketers)

Data analysis (replacing business intelligence teams)

Customer service (via AI agents and chatbots)

Back-office workflows (legal review, accounting, recruiting)

Goldman Sachs estimates generative AI will raise U.S. labor productivity by approximately 15 percent at full adoption. The compounding effect on solo operators is larger than on incumbents because solos start without the fixed overhead AI is now substituting away. Bessemer’s Vertical AI playbook maps the new pattern: products that solve a specific workflow inside a single industry, built by small teams, replacing horizontal SaaS budgets with vertical AI agents. Sequoia’s investment teams now underwrite what they call agentic leverage, the ability of one or two operators to produce the output of a 10-person team using orchestrated AI agents.

3. Payment Systems as Financial Rails

Stripe and Square reduced transaction friction to near-zero. Stripe operates in more than 135 countries with more than 135 supported currencies and processes hundreds of billions of dollars annually. Square’s 2024 gross payment volume reached approximately $180 billion across small and medium businesses, with 34 percent of users running solo operations. The APIs enable instant global payments, recurring billing, and multi-party revenue splits. Those functions once required banking partnerships, merchant accounts, and dedicated accounting teams.

VI. The Operator Economy in Practice

From Gig Workers to Creators

The gig economy commoditized labor. Uber drivers, DoorDash couriers, and TaskRabbit workers were paid for fungible time. The creator economy inverted the pattern. Individuals build audiences around specific skills and monetize through courses, subscriptions, products, and services. Platforms like Substack and Patreon function as a business in a box for solo operators.

AI-Enabled Scaling

A graphic designer in 2026 uses Midjourney for rapid prototyping, Calendly for client scheduling, QuickBooks AI for invoicing, and Claude for client communications. The operation reaches small-agency capability without small-agency headcount. The capital efficiency of a one-person operation built on AI tools is roughly 10 to 50 times higher than a traditional startup, which is why Sequoia, Bessemer, and a16z are repricing solo founders as a real venture category.

Case Study: The History-Informed Operator

A historian launches a research service in three moves:

They source archival data via digitized collections, removing the pre-internet access barrier that locked specialist knowledge inside university libraries

They use Perplexity, Claude, and ChatGPT to synthesize sources at scale

They monetize through LinkedIn thought leadership and a Calendly-Zoom-Stripe stack that handles scheduling, delivery, and payment

The operation encapsulates 500 years of economic evolution in a single moment. It carries the communal knowledge-sharing logic of guilds, the specialization of industrial crafts, and the platform-enabled autonomy of the digital age.

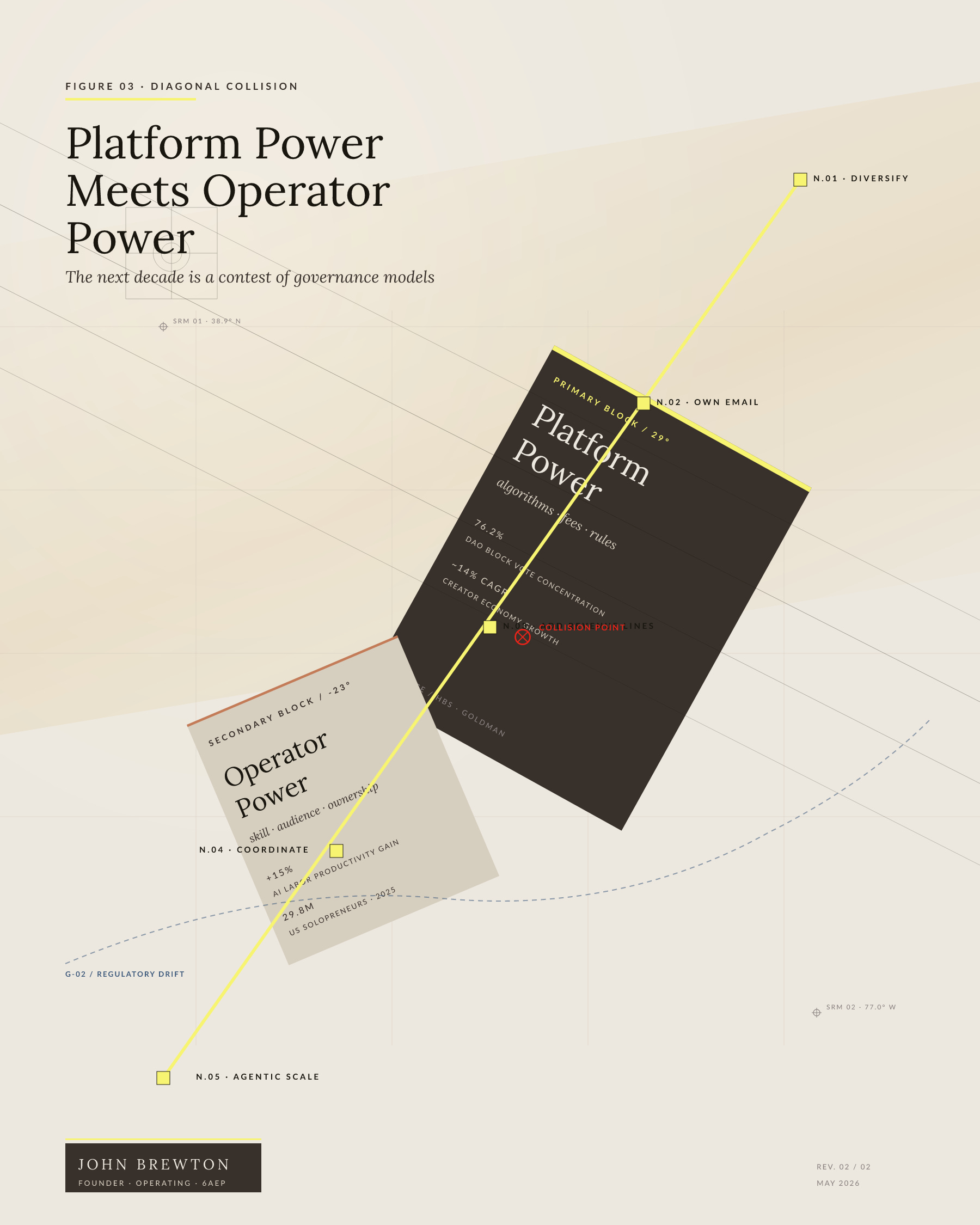

VII. Historical Parallels and Critical Differences

History supplies both the precedent and the warning. The medieval commons and 19th-century cooperatives were governed by shared rules and mutual oversight. Today’s platforms are global in reach and centrally controlled. Algorithms and policy changes are opaque. Risk and reward were once distributed across a community. The platform economy concentrates risk on the individual operator and offers little recourse.

Power dynamics have shifted. Historical cooperatives operated on democratic principles. Members had a voice and a vote. Modern platforms operate more like feudal arrangements. They provide infrastructure in exchange for data, fees, and compliance with unilaterally imposed rules. Harvard Business School research on DAO governance finds that even ostensibly decentralized autonomous organizations concentrate voting power, with 76.2 percent of voting power held by block voters. The Belfer Center’s policy work shows the gap between the decentralized governance ideal and the centralization that emerges in practice. The scale is unprecedented. So is the concentration of control.

The challenge is making sure the digital commons of the 21st century do not replicate the inequities of the past under the cover of innovation. The question is whether we are democratizing entrepreneurship or shifting old power structures into new forms of extraction. The honest answer is both, in different proportions in different sectors. The policy work of the next decade will determine which proportion wins.

Figure 03. Platform Power Meets Operator Power. The next decade is a contest of governance models.

Inequality and Access

The operator economy promises autonomy and opportunity. It is not a universal equalizer. Access to digital tools, stable internet, and platform skills remains unevenly distributed across countries and within them. Many operators face income volatility, lack of benefits, and the constant risk of changes to platform rules.

Barriers persist. Digital literacy, reliable internet, and a financial cushion to absorb early-stage uncertainty exclude many potential operators. The most successful platform entrepreneurs come from privileged backgrounds with networks, capital, and risk tolerance already built in.

Platform dependency creates new vulnerabilities. Academic research on platform-mediated work shows that algorithm changes can devastate a creator’s income overnight. Recent earnings analysis using Patreon data shows that algorithmic curation concentrates earnings at the top and pulls income away from a creator middle class. The promise of autonomy becomes algorithmic management more invasive than traditional employment. For some operators, the dream becomes a struggle for survival with less security than a job once provided. The Pew Research Center’s 2017 expert survey cataloged the risks early. Most of them are now playing out.

IX. Implications and Future Trajectories

Opportunities

Democratized entrepreneurship. Lowered barriers enable global participation

Flexibility. Operators choose projects that align with values and expertise

Economic resilience. Diversified income streams buffer market shocks

Challenges

Platform dependence. Algorithm changes can disrupt livelihoods overnight

Regulatory gaps. Labor and tax systems lag the new business models

Inequality. Access to tools remains uneven globally

The Future of Companies

Decentralized autonomous organizations point toward a future in which operators collectively govern shared infrastructure. The early DAO data shows the gap between the ideal and the implementation. AI agents will take on administrative and operational tasks, freeing operators to focus on creative and strategic work. The boundary between a company and a network of cooperating operators continues to blur.

A Roadmap for Aspiring Operators

Resilience and strategic thinking are the two requirements. The tools change. The principles do not.

Build Antifragility

Diversify presence across multiple platforms to reduce single-point-of-failure risk

Cultivate direct relationships with audience and clients. Email capture is the most durable layer

Invest in continuous learning to stay ahead of automation and market shifts

Use Technology Wisely

Treat AI as an assistant, not a substitute for judgment and creativity

Develop the human skills AI does not replicate: emotional intelligence, creative problem-solving, relationship building

Build systems that scale without compromising quality or authenticity

Advocate for Better Systems

Support platforms with transparent algorithms and fair revenue sharing

Push for portable benefits that travel with workers across platforms

Coordinate with other operators to negotiate fairer terms

Push regulators toward frameworks that protect operators without stifling innovation

Think Long-Term

Treat platform participation as one element of a strategy, not the whole strategy

Build owned assets (email lists, websites, intellectual property) alongside platform presence

Develop multiple revenue streams to absorb platform volatility

Conclusion

The shift toward an operator-centric economy is both new and deeply rooted in economic history. From medieval commons to digital platforms, the drive to democratize production and exchange has reshaped business across centuries. Individuals now wield capabilities once reserved for corporations. AI and global connectivity carry the cost curve the rest of the way down.

The shift is neither inevitable nor universally beneficial. The operator economy’s promise depends on actively addressing inequities, dependencies, and risks. We are not entering an era of side hustles. We are watching the rebirth of the company. Smaller. Nimbler. Human in scale and decidedly more so in character. Whether the evolution empowers operators or extracts from them depends on the choices made in the next ten years.

The Operator age is here. It belongs to anyone ready to build. Building wisely requires understanding both the opportunities and the obstacles.

What’s Next

The operator and creator economies are not static. They are reshaping the nature of work, entrepreneurship, and value creation in real time. Several frontiers matter most.

Regulatory frameworks will need to protect operators without strangling the innovation that produced them. New business models and forms of collective action will emerge as more individuals operate as companies of one. Household income structures will shift as creator-economy channels move from supplementary to primary. The skills and safeguards that allow operators to thrive in an environment where autonomy and precarity coexist will define the next decade of work.

One frontier matters most for this community. Polymaths, individuals who blend expertise across disciplines, will set the pace as AI takes on specialized tasks. The ability to connect ideas, synthesize knowledge, and innovate across domain boundaries becomes the most valuable skill of the next decade.

At Operating, I examine the future of company structure and the evolution of digital platforms, the realities of platform dependence, the strategies that will define operator success, and the resurgence of polymathic talent as a primary driver of innovation and adaptability.

I want your input. What are you seeing in your own work and industry?

Whether you are already operating as a company of one or are considering the move.

What challenges and opportunities do you foresee as the operator and creator economies mature?

Whether you consider yourself a polymath or are working to become one, consider how the ability to connect ideas across fields is shaping your work.

Thank you for reading.

John

John Brewton documents the history and future of operating companies at Operating by John Brewton. He is an economics graduate of Harvard University and the University of Chicago. After selling his family’s B2B industrial distribution company in 2018, he has been helping business owners, founders, and investors optimize their operations ever since. His frameworks have generated over +$250M in enterprise value. He still cringes at his early LinkedIn posts.

APPENDIX: RESEARCH SOURCES

All sources are drawn from elite publications, top academic centers, and institutional investment research. Each carries a credibility tag.

A. Historical Foundations (Section I)

Elinor Ostrom: Governing the Commons [PEER-REVIEWED] Cambridge University Press, 1990. Nobel Memorial Prize in Economic Sciences, 2009. Documents more than 800 common-pool resource governance arrangements. Cambridge University Press

Elinor Ostrom Profile: Stanford GSB [INSTITUTIONAL] Background on Ostrom’s analytical framework and its application to modern commons. Stanford GSB Insights

David T. Beito: From Mutual Aid to the Welfare State [PEER-REVIEWED] University of North Carolina Press. Comprehensive history of fraternal societies and friendly societies, 1890-1967. UNC Press

Einav and Farronato: Peer-to-Peer Markets [PEER-REVIEWED] NBER Working Paper 21496. Analysis of digital marketplaces from eBay through Airbnb and Uber. NBER

eBay Founding History [EDITORIAL] Britannica Money. Pierre Omidyar founded AuctionWeb in September 1995. Reputation systems became the trust infrastructure for the platform economy. Britannica

B. The 2008 Crisis (Section II)

Katz and Krueger: The Rise and Nature of Alternative Work Arrangements [PEER-REVIEWED] NBER Working Paper 22667. Alternative work arrangements grew from 10.7% to 15.8% of US workforce, 2005-2015. NBER · Harvard Kennedy School (Katz)

Hall and Krueger: Analysis of the Labor Market for Uber’s Driver-Partners [PEER-REVIEWED] ILR Review, 2018. The first comprehensive analysis of platform driver economics. ILR Review (SAGE) · NBER version

Resolution Foundation: Just the Job or a Working Compromise [INSTITUTIONAL] UK self-employment accounted for 45% of all employment growth from March 2008. Self-employment grew by 650,000 to 4.5 million. Resolution Foundation

ONS: Trends in Self-Employment in the UK [INSTITUTIONAL] UK self-employment rose from 3.8 million in 2008 to 4.6 million in 2015. ONS

C. COVID-19 and the Operator Acceleration (Section III)

Barrero, Bloom, Davis: The Evolution of Work from Home [PEER-REVIEWED] Hoover Institution / Stanford. The seminal longitudinal WFH dataset (SWAA). Hoover Institution · American Economic Association

Stanford GSB: The Pandemic Blew Up the American Office [INSTITUTIONAL] Stanford GSB Insights. Bloom et al. on the durable structural shift in workplace location. Stanford GSB

Gratton: Seven Truths About Hybrid Work and Productivity [EDITORIAL] MIT Sloan Management Review. Teams together 23-40% of the time outperform on multiple dimensions. MIT Sloan Review

Aksoy et al.: Working from Home Around the World [PEER-REVIEWED] NBER Working Paper 30446 and Brookings Papers on Economic Activity. International comparison of remote work persistence. NBER · Brookings

McKinsey: Freelance, Side Hustles, and Gigs [INSTITUTIONAL] American Opportunity Survey. 36% of US workforce (≈58M) identified as independent workers in 2022, up from 27% in 2016. McKinsey

US Census Bureau: Business Owners and the Self-Employed [PEER-REVIEWED] Working paper CES-25-60. Non-employer business growth peaked at 4.9% in 2021 and 4.7% in 2022, fastest in nearly two decades. Census Bureau

D. The Creator Economy (Section IV)

Goldman Sachs Research: The Creator Economy Could Approach Half-a-Trillion Dollars by 2027 [INSTITUTIONAL] $250B today, projected $480B by 2027. ~14% CAGR. 50M global creators growing 10-20% annually. Goldman Sachs

Li Jin: The Creator Economy Needs a Middle Class [EDITORIAL] Harvard Business Review, December 2020. Diagnosis of income concentration and prescription for platform mechanics. HBR

Li Jin: The Passion Economy and the Future of Work [INSTITUTIONAL] Andreessen Horowitz. The thesis that distinguished the creator economy from the commoditized gig economy. a16z · a16z 16 Key Metrics

HBR: How Your Business Should Tap into the Creator Economy [EDITORIAL] Harvard Business Review, May 2024. Smaller creators (under 50,000 followers) account for 76% of all TikTok creators and 96% on Instagram. HBR

E. Platform Stack and AI Infrastructure (Sections V-VI)

Stripe: Global Payment Processing Platform [INSTITUTIONAL] Stripe operates in 135+ countries, supports 135+ currencies, and processes hundreds of billions annually. Stripe

Bessemer Venture Partners: Building Vertical AI Playbook [INSTITUTIONAL] The investment thesis for vertical AI companies replacing horizontal SaaS budgets. Bessemer

Bessemer: Everything Everywhere All AI [INSTITUTIONAL] Bessemer’s AI investment thesis book, 2024. Bessemer

Goldman Sachs Research: How Will AI Affect the Global Workforce [INSTITUTIONAL] Generative AI will raise US labor productivity by approximately 15% at full adoption. Goldman Sachs

Morgan Stanley: AI and Jobs: Labor Market Impact Echoes Past Tech Transitions [INSTITUTIONAL] Historical analogues for AI displacement and re-employment. Morgan Stanley

F. Historical Parallels and Platform Governance (Section VII)

Harvard Business School: Centralized Governance in Decentralized Organizations [PEER-REVIEWED] Working paper. Block voters control 76.2% of voting power in DAO governance decisions. HBS

Harvard Belfer Center: Decentralized Autonomous Organizations and Policy Considerations [INSTITUTIONAL] Technology and Public Purpose Project policy brief, 2025. Belfer Center

The Governance of DAOs: Contributor Voting Power Analysis [PEER-REVIEWED] Empirical analysis showing concentrated voting power across DAO ecosystems. arXiv

G. Platform Dependency and Algorithmic Risk (Section VIII)

Pew Research Center: Code-Dependent: Pros and Cons of the Algorithm Age [INSTITUTIONAL] Expert survey of algorithmic governance and its effects on workers. Pew Research

Dependence and Precarity in the Platform Economy [PEER-REVIEWED] Theory and Society. Worker satisfaction and earnings volatility across platforms. Springer / Theory and Society

Rich-Get-Richer? Platform Attention and Earnings Inequality [PEER-REVIEWED] Earnings analysis using Patreon data. Algorithmic curation concentrates income at the top. arXiv

Content Creators Between Platform Control and User Autonomy [PEER-REVIEWED] Analysis of how creators adapt income strategies to algorithmic changes. PMC / NCBI

All findings drawn from elite publications (NYT, FT, WSJ, Economist, HBR, MIT), top academic centers (Harvard, Stanford, Princeton, Chicago Booth, LSE, NBER), and institutional research (Goldman Sachs, Morgan Stanley, McKinsey, Bessemer, Andreessen Horowitz, Resolution Foundation, Pew Research, Brookings, Hoover).

John Brewton · Founder · Operating · 6AEP

Nice to showcase the evolution with historical events. And it feels great to be an operator

Smart historical framing.