Operating Economics: The Optimization Company

Amazon’s Triumphant Operational Reckoning: What Two Years of Earnings Reveal About the Next Corporate Model

New to Operating by John Brewton?

Check out these reader favorites:

Earning’s Reports

On the morning of July 31st, 2025, Amazon reported quarterly earnings that on paper represented triumph: revenue up 13% year-over-year to $167.7 billion, earnings per share of $1.68 crushing the consensus estimate by 26%, and operating income reaching $19.2 billion. Yet by market close the following day, the stock had plummeted 8.3%, its worst post-earnings reaction in years. Wall Street’s verdict was unambiguous: the company’s guidance for the subsequent quarter implied that Amazon’s unprecedented capital expenditure, despite driving revenue growth, was compressing margins without delivering the operating leverage investors had been promised.

Just three months later, Amazon has announced plans to eliminate 14,000 corporate positions, part of an expected reduction of up to 30,000 jobs, representing roughly 10% of its white-collar workforce. The timing, two days before third-quarter earnings, is hardly coincidental. It echoes CEO Andy Jassy’s explicit, strategic commitment in June that “in the next few years, we expect that [AI] will reduce our total corporate workforce.”

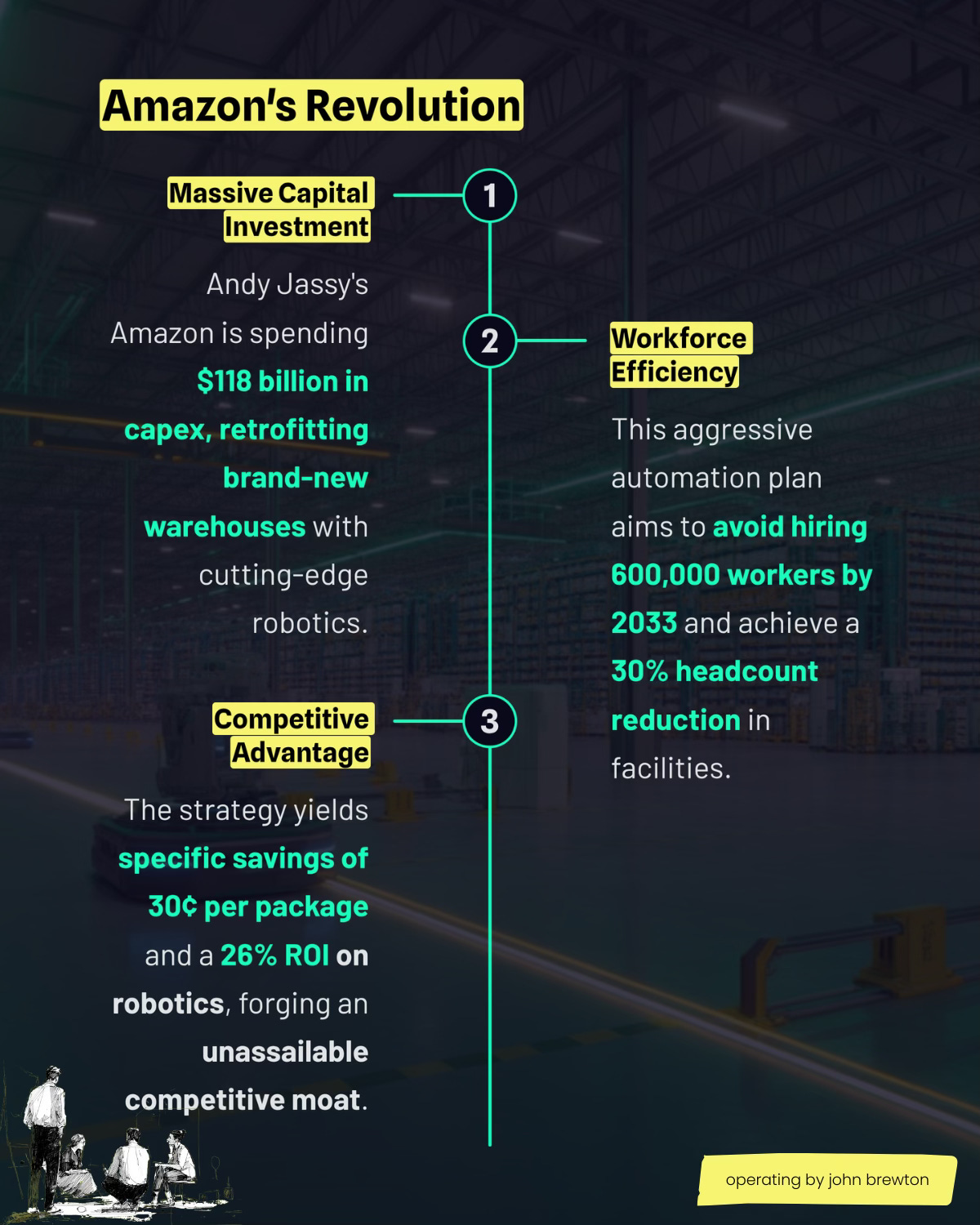

Beneath these headlines is an instructional transformation story. Internal documents obtained by The New York Times revealed that Amazon expects to avoid hiring more than 600,000 workers by 2033, even as it projects sales volumes to double, achieving this through automation of 75% of its warehouse operations. Combined with over $100 billion in annual capital expenditure (40% higher than 2024), the company is executing one of the most ambitious labor-to-capital substitution strategies in corporate history.

The financial results of the past two years tell the story of this transition with unusual clarity. It is a cost optimizing blueprint for a fundamentally different kind of corporation: one where growth and headcount are not as closely aligned, where capital intensity becomes the primary competitive driver, and where traditional assumptions about the relationship between firm success and job creation appear to be diverging.

Amazon's earnings trajectory offers an invaluable case study for strategists and operators like me, most concerned with understanding the future of how companies operate successfully. The question is no longer whether technology enables companies to grow while shrinking their workforce (Amazon has demonstrated that it does, as has Meta in recent times) but rather what this portends for the future of companies, markets, and successful operating execution.

From Cost-Cutting to Capital Intensity

The inflection point came in the fourth quarter of 2023. After years of pandemic-era overhiring followed by painful retrenchment, Amazon reported operating income of $13.2 billion and net income of $10.6 billion, more than triple the prior year’s profit. The stock surged 9.5% in a single day. Investors were witnessing the fruits of Andy Jassy’s unrelenting efficiency campaign: substantial layoffs, the regionalization of the fulfillment network into eight autonomous zones, and an obsessive focus on cost per unit shipped.

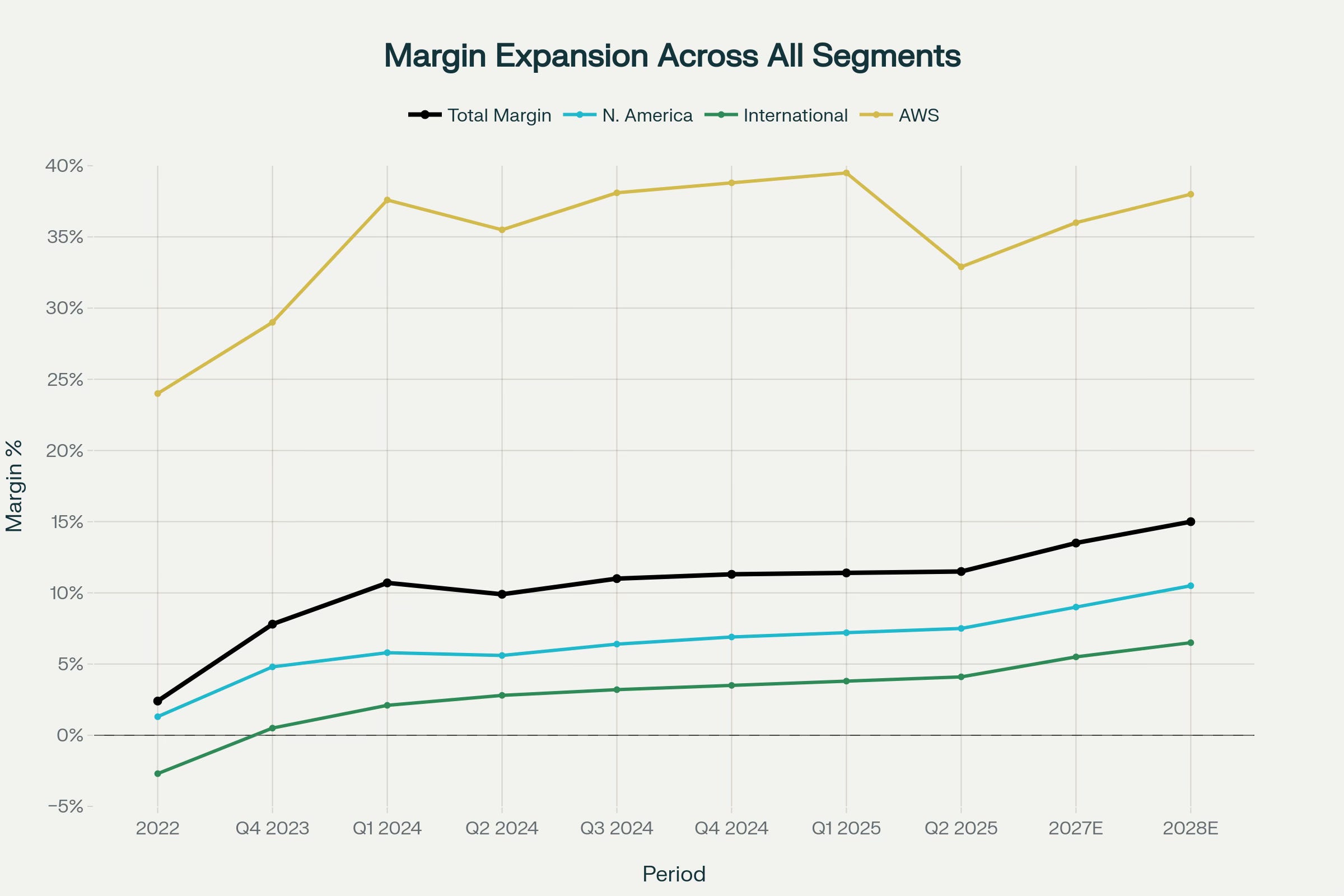

Throughout 2024, this margin expansion story continued. Operating margin, which had languished at 2.4% in 2022, reached 11.3% by year’s end, the highest sustained level in company history. Each quarterly earnings call reinforced the narrative: 13% revenue growth in Q1, 10% in Q2, 11% in Q3, with operating income soaring 219%, 88%, and 56% respectively. Amazon Web Services, the company’s profit engine, stabilized at 17-19% growth after several quarters of deceleration, while advertising revenue climbed 20-26% quarterly.

Systematic Margin Transformation: Amazon achieved operating margin expansion across every business segment from 2022 through 2025. Total company margins quintupled while AWS maintained 32-40% profitability, North America retail turned structurally profitable above 7%, and International finally crossed into positive territory, all amid record capital spending.

Wall Street’s response, however, was bifurcated. Despite consistent earnings beats, the stock fell after four of the eight quarters from Q4 2023 through Q2 2025. The market had begun focusing less on backward-looking results and more on forward guidance, particularly operating income projections. When Q2 2025 guidance implied margins below expectations, despite the massive revenue beat, analysts concluded that Amazon’s escalating capital spending was beginning to overwhelm its operational efficiency gains.

The Paradox of Success: Amazon’s operating margins climbed steadily from 7.8% to 11.5% between Q4 2023 and Q2 2025, yet stock reactions remained volatile—falling sharply after beats when guidance disappointed.

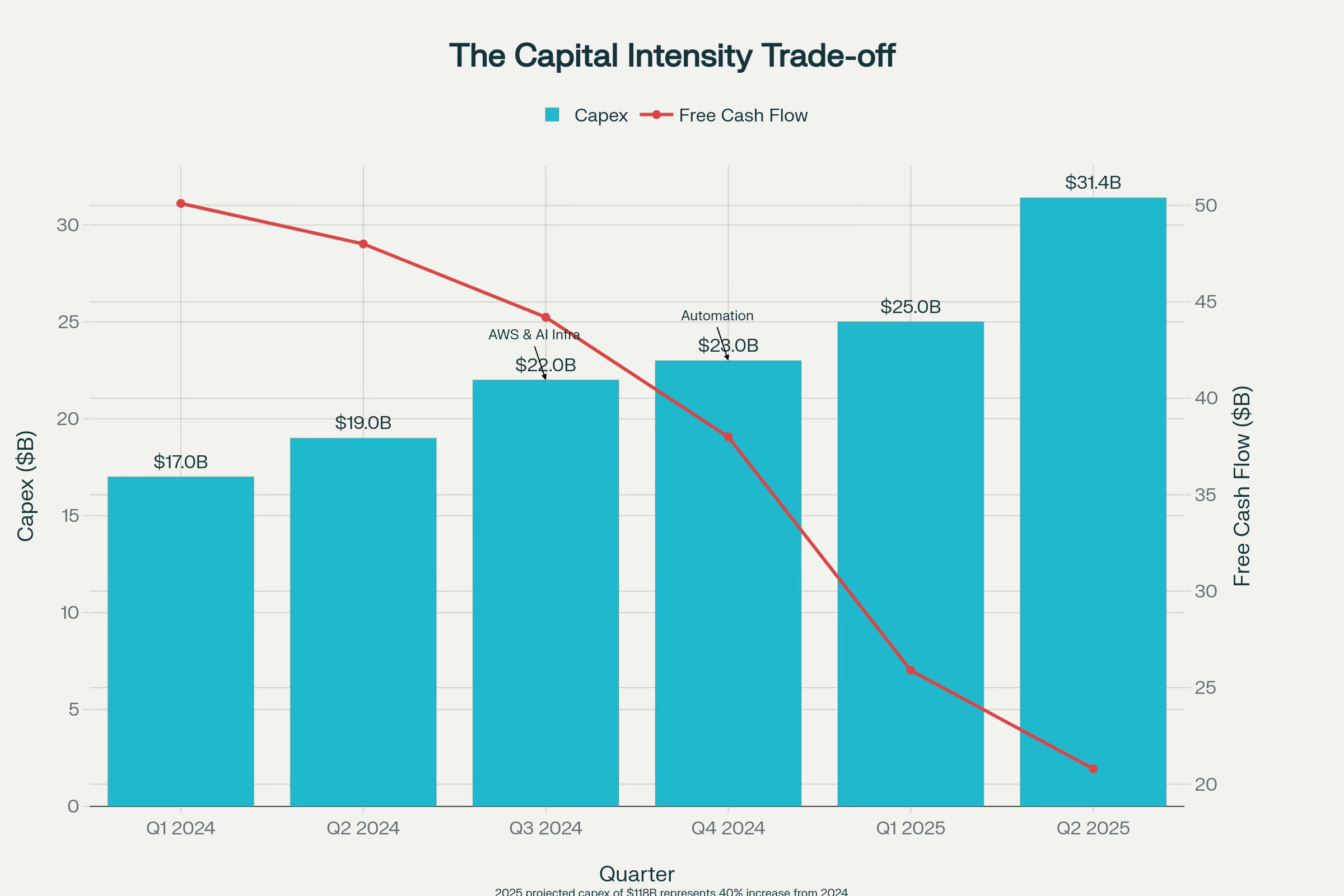

The numbers bore this out. Capital expenditures hit $31.4 billion in Q2 2025 alone, running at a $125 billion annual rate. Free cash flow, which had reached $50 billion on a trailing twelve-month basis in early 2024, compressed to roughly $20 billion by mid-2025, a 60% decline. Amazon was explicitly trading near-term cash generation for long-term structural transformation.

The strategy's duality makes it striking. The capital deployment flows into two parallel but complementary initiatives: AWS data center expansion to address AI infrastructure demand and warehouse robotics to systematically eliminate human labor from physical operations. The former aims to capture the “once-in-a-lifetime” artificial intelligence opportunity. The latter pursues something far more radical: proving that a business processing billions of physical items annually can operate with a fraction of its current workforce.

The Economic Architecture of Automated Operations

Amazon is an operation being reimagined from first principles. At their Shreveport, Louisiana, fulfillment center, which opened in 2024, employment is already 25% below what it would have been without automation. By year two, the target is 50% below the traditional staffing model. The Stone Mountain, Georgia, facility (built only five years ago) is being retrofitted at significant expense to process 10% more volume with 1,200 fewer workers, a 30% headcount reduction.

The economics are compelling. Amazon projects savings of 30 cents per unit processed through automation, a modest figure on its face, but one that translates to billions in annual cost avoidance when multiplied across the company’s volume. A $10 billion robotics investment through 2027 is expected to generate $12.6 billion in labor cost savings, representing a 26% return. With warehouse wages averaging $19.50 per hour and typical tenure measured in months, not years, the payback period for robotic systems amortized over five to seven years pencils out to roughly two to three years, an internal rate of return that few corporate investments can match.

The Economic Logic of Automation: Amazon’s $10 billion warehouse robotics investment through 2027 generates a 26% return on investment through labor cost avoidance—30 cents saved per item processed, 600,000+ jobs avoided by 2033, and a payback period of just 2-3 years.

They’re not experimenting. Amazon has surpassed one million deployed robots in its operations network. The company’s acquisition of Kiva Systems in 2012 for $775 million, considered expensive at the time, now appears prescient. Those early investments created the foundation for increasingly sophisticated systems: robotic arms that can handle items of varying shapes and weights, autonomous mobile robots that transport inventory without human guidance, and AI-powered systems that optimize routing and picking sequences in real-time.

Critically, these are not tools that augment human labor but rather systems designed to eliminate it. Where traditional fulfillment centers employed 2,000 workers, new automated facilities target 800, with the majority of the remaining positions either targeting specialized technicians or temporary workers for peak periods.

Daron Acemoglu, the MIT economist whose research on automation and employment has become foundational, observed to The New York Times:

“Nobody else has the same incentive as Amazon to find the way to automate... Once they work out how to do this profitably, it will spread to others, too”.

His prediction: Amazon will become “a net job destroyer, not a net job creator.” This stands in direct contradiction to classical economic theories that assume historical waves of automation create more jobs than they eliminate.

The distinction lies in intentionality. Previous industrial automation was often a byproduct of productivity improvements. Amazon’s strategy is explicitly designed to avoid employment growth even as volumes surge. The company’s projection of doubling sales by 2033 without workforce expansion implies labor productivity (measured as revenue per employee) must double over eight years, a sustained rate without modern precedent.

The Decoupling of Growth and Employment: Amazon projects doubling sales volume by 2033 while reducing total workforce from 1.6 million to approximately 1 million. The widening gap represents unprecedented labor productivity in modern retail.

Operating History: How Carnegie Used Capital to Change an Industry

Link here to exclusive paid subscriber coverage of the Andrew and Amazon historical parallels

Wall Street’s Education: When Beats Become Disappointments

The tension between Amazon’s strategic vision and market expectations crystallized most clearly in the second quarter of 2025. The results themselves were exceptional: revenue growth accelerated to 13%, AWS revenue reached a $123 billion annual run rate (up 17.5%), advertising climbed 23%, and EPS of $1.68 demolished estimates. Brian Olsavsky, Amazon’s CFO, emphasized that AWS infrastructure constraints, not demand weakness, were limiting growth, and that massive capital deployment would alleviate these bottlenecks in subsequent quarters.

Yet Q3 operating income guidance of $15.5 billion to $20.5 billion, with a midpoint of $18 billion, fell short of the Street’s $19.5 billion expectation. Analysts immediately grasped the implication: Amazon’s operating margin was compressing from 11.5% in Q2 to roughly 10-11% in Q3, despite all the efficiency initiatives. The capital intensity required to build data centers, install GPU clusters, and retrofit warehouses was overwhelming the cost savings from labor reduction, at least in the near term.

The market reaction was direct. The stock fell 8.8% over two trading sessions, wiping out nearly $180 billion in market capitalization. Analysts who had maintained “Strong Buy” ratings scrambled to explain the divergence. RBC Capital Markets called it “an uncharacteristic setback” and predicted AWS would reaccelerate once new capacity came online. Wedbush Securities was less forgiving, warning that “AWS’s image as an AI leader may be taking a hit” as Microsoft Azure and Google Cloud posted growth rates nearly double Amazon’s.

This pattern, beats followed by selloff, has become characteristic of Amazon’s relationship with investors. The company beat earnings estimates in all eight quarters from Q4 2023 through Q2 2025, yet the stock fell after four of these reports. What changed was the market’s recognition that Amazon had entered a fundamentally different phase. The margin expansion era of 2023-2024, driven by cutting costs from the existing business, had given way to a capital deployment era where billions flow out before returns materialize.

The echo of this moment reaches back nearly three decades. In his 1997 letter to shareholders, Amazon’s first as a public company, Jeff Bezos established what he called an “It’s All About the Long Term” philosophy that would define the company’s decision-making for decades. He wrote explicitly:

“We will continue to make investment decisions in light of long-term market leadership considerations rather than short-term profitability considerations or short-term Wall Street reactions.”

More provocatively, when asked about profitability in a 1997 New York Times interview, Bezos declared: “We are not profitable. We could be. It would be the easiest thing in the world to be profitable. It would also be the dumbest. We are taking what might be profits and reinvesting them in the future of the business.” He was asking investors to accept years, potentially a decade, of losses in exchange for market leadership and scale that would eventually generate substantial returns.

Bezos was so committed to this compact that he attached the 1997 letter to every subsequent annual report through 2020, ensuring each new cohort of shareholders understood the terms of engagement. In his 2003 letter, he wrote: “Long-term thinking is both a requirement and an outcome of true ownership. Owners are different from tenants.” The philosophy enabled Amazon to pursue the “Get Big Fast” strategy that prioritized growth over profitability, building fulfillment infrastructure and expanding into new categories while operating at losses that would have destroyed most companies.

The parallel to AWS’s own history is instructive. Amazon Web Services required years of heavy investment before becoming profitable, ultimately generating 32-40% operating margins that now contribute over $50 billion annually in operating income despite representing only 18% of revenue. The bet paid off spectacularly: AWS transformed from an internal cost center to a business generating more operating income than Amazon’s entire North American retail operation. Management is betting that robotics and AI will follow a similar J-curve: near-term margin pressure in exchange for a structurally superior cost base by 2027-2028.

The J-Curve Investment Cycle: Amazon’s capital expenditures surged 40% to $118-125 billion annually in 2025, driven by AWS infrastructure and warehouse automation, while free cash flow compressed from $50 billion to $20 billion. Management is explicitly trading near-term cash generation for long-term structural transformation, echoing the AWS buildout years.

Yet there is a crucial difference that explains Wall Street’s ambivalence. AWS built entirely new revenue streams in the cloud infrastructure market that grew from nearly zero to over $200 billion globally in less than two decades. Warehouse automation, by contrast, reduces costs on existing revenue. If successful, it improves profitability without expanding the top line. The savings from eliminating 600,000 positions over eight years, even at $12.6 billion cumulatively, pale in comparison to the $100+ billion in annual revenue AWS now generates.

This makes the current strategy simultaneously lower-risk (Amazon retains its core retail business regardless of automation outcomes) and lower-upside (cost savings, while substantial, cannot match the transformative impact of a new $100 billion+ revenue stream). Where Bezos asked 1997 shareholders to tolerate losses while building a new category, Jassy is asking 2025 shareholders to tolerate margin compression while optimizing an existing one. The former bet on market creation; the latter bets on operational excellence.

What remains consistent across both eras is Amazon’s willingness to absorb near-term investor pain for long-term structural advantage. Bezos built this tolerance into the company’s DNA, writing in 1997: “When forced to choose between optimizing the appearance of our GAAP accounting and maximizing the present value of future cash flows, we’ll take the cash flows.” The question facing today’s investors is whether they still possess the patience that Bezos demanded, and whether the automation bet, unlike AWS, offers rewards commensurate with that patience.

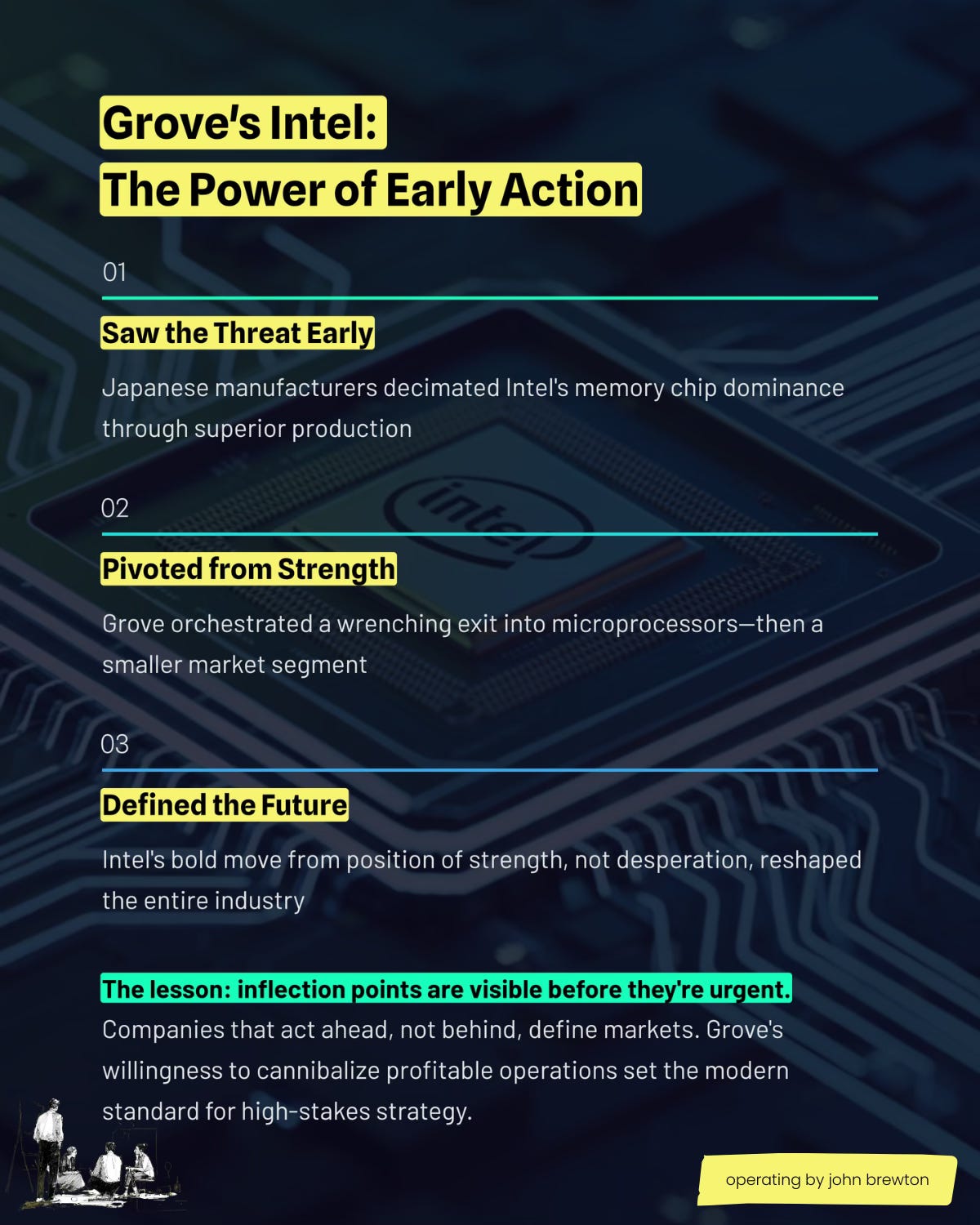

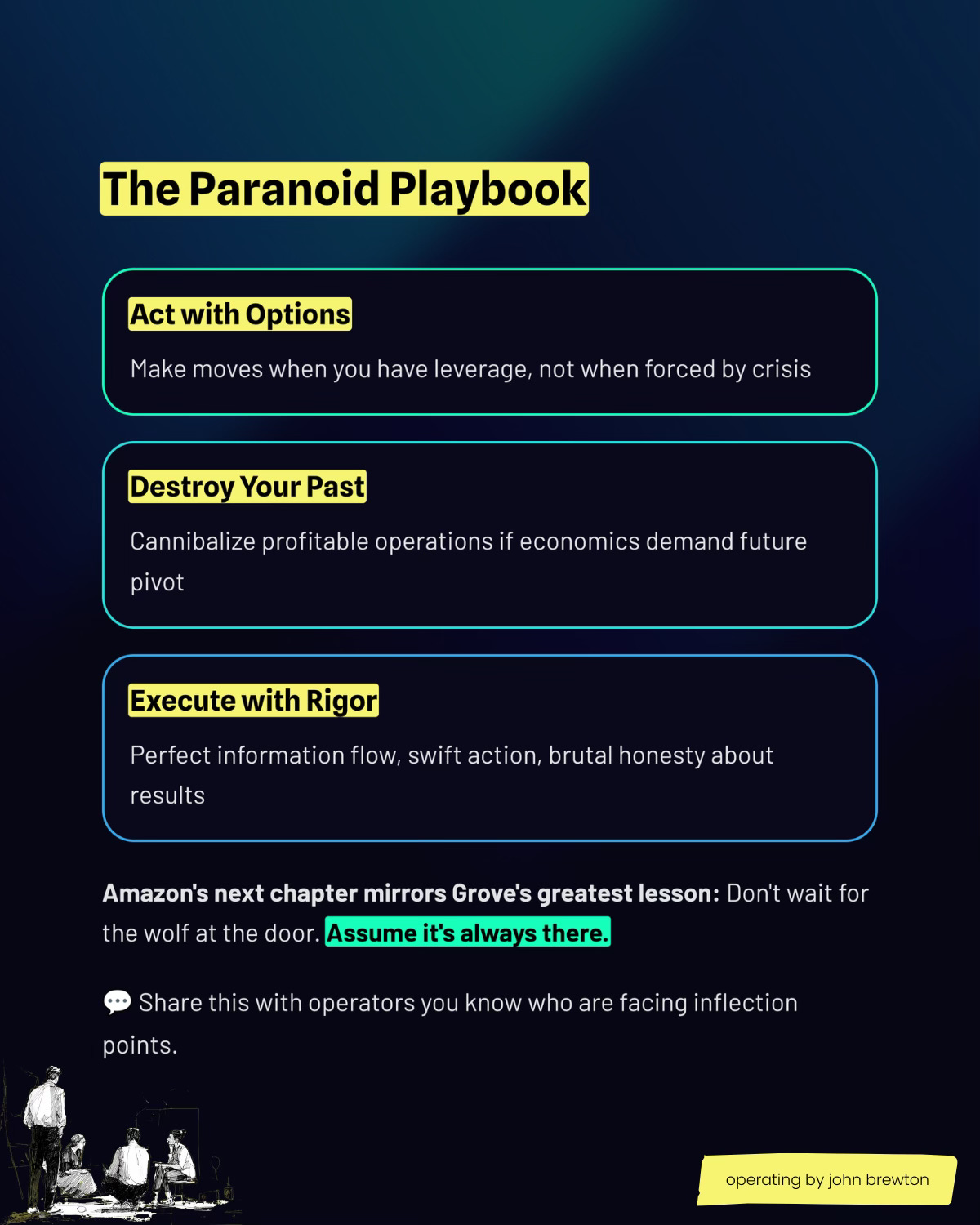

Operating History: Only the Paranoid Survive: Grove, Inflection Points, and Acting from Strength

Link here to exclusive paid subscriber content that goes deep on the Amazon-Andy relationship.

Four Strategic Operating Principles

Amazon’s transformation, viewed through the lens of its financial results and operational decision making, yields four principles that are applicable beyond the company itself, and essential for all operators to understand.

One

Model the capital-labor substitution frontier with precision. Amazon’s automation decisions are not driven primarily by technological feasibility, most warehouse tasks have been technically automatable for years, but by detailed financial modeling. Internal documents show exact break-even calculations:

At what wage level does robotics become economically superior?

What is the payback period for specific automation investments?

How do these economics vary by facility type, throughput volume, and labor market conditions?

This approach treats automation as a capital allocation decision, not an engineering challenge. The implications are significant: automation accelerates not when technology improves but when the factor price ratio shifts. Post-pandemic wage pressure and labor scarcity tipped numerous tasks past the automation threshold, accelerating deployment timelines that had existed in theory for years. Strategic operators should similarly map their own substitution frontiers, identifying which roles become automatable at which cost structures, rather than waiting for technology to “mature.”

Two

Sequence investments for compound returns. Amazon’s phasing is deliberate: regionalization of fulfillment (2021-2023) to reduce shipping distances and improve speed, followed by robotics deployment (2024-2027) to amplify those gains, followed by AI coordination systems (2025-2028) to optimize the automated network. Each wave creates infrastructure for the next while maintaining adequate profitability to fund subsequent phases.

The alternative, attempting simultaneous transformation, would have collapsed operating margins below levels Wall Street would tolerate, potentially constraining the company’s ability to raise capital or defend against activist investors. By maintaining 10-11% operating margins throughout the transition, Amazon preserves strategic flexibility. This sequencing discipline, more than any individual technology, distinguishes successful large-scale transformations from value-destroying restructurings.

Three

Third, exploit platform economics to decouple growth from headcount. Amazon’s ability to project doubling sales without workforce expansion depends critically on its platform model. Growth increasingly comes not from Amazon’s direct operations but from third-party sellers (now 62% of units sold), AWS customers, and advertisers. The company earns fees, commissions, and service charges on economic activity it enables but does not directly execute.

Third-party seller services generated $156 billion in 2024, growing 11% quarterly in 2025, while advertising reached $63 billion annually with 20%+ growth. Both carry significantly higher margins than first-party retail. Combined, they represent a structural shift from Amazon as retailer (employing people to sell things) to Amazon as infrastructure provider (collecting rent on others selling things). This platform transition is what makes the automation strategy economically viable: revenues grow through the ecosystem while direct employment shrinks through automation.

For strategists in other industries, the principle generalizes: businesses that can capture value from activity they orchestrate rather than execute directly can scale with minimal marginal labor. This explains Big Tech’s valuation premiums, AWS, Google Cloud, and Meta’s advertising platform achieve revenue-per-employee ratios 3-5x traditional businesses. Amazon’s bet is that platform economics can be imported into physical operations through sufficient automation.

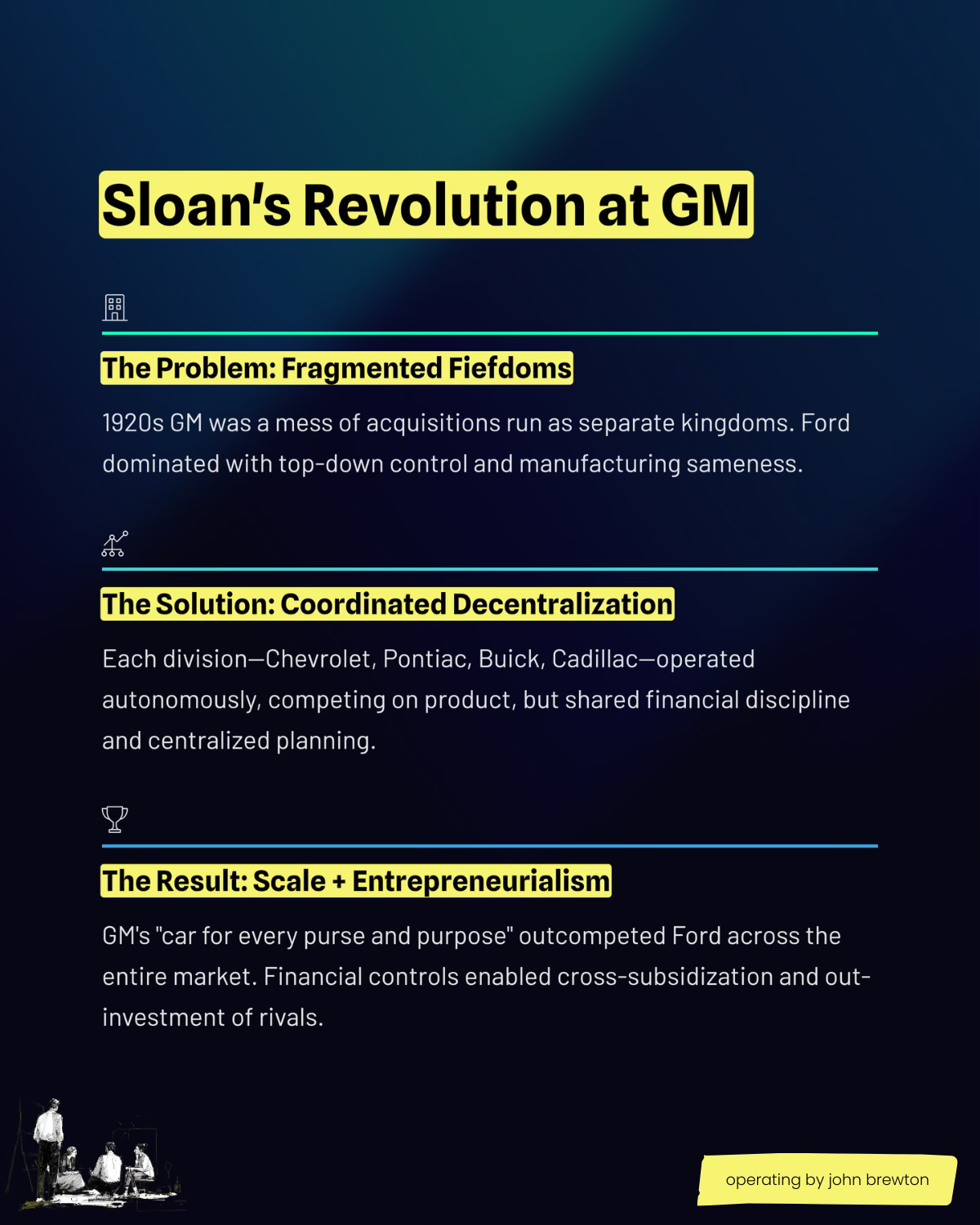

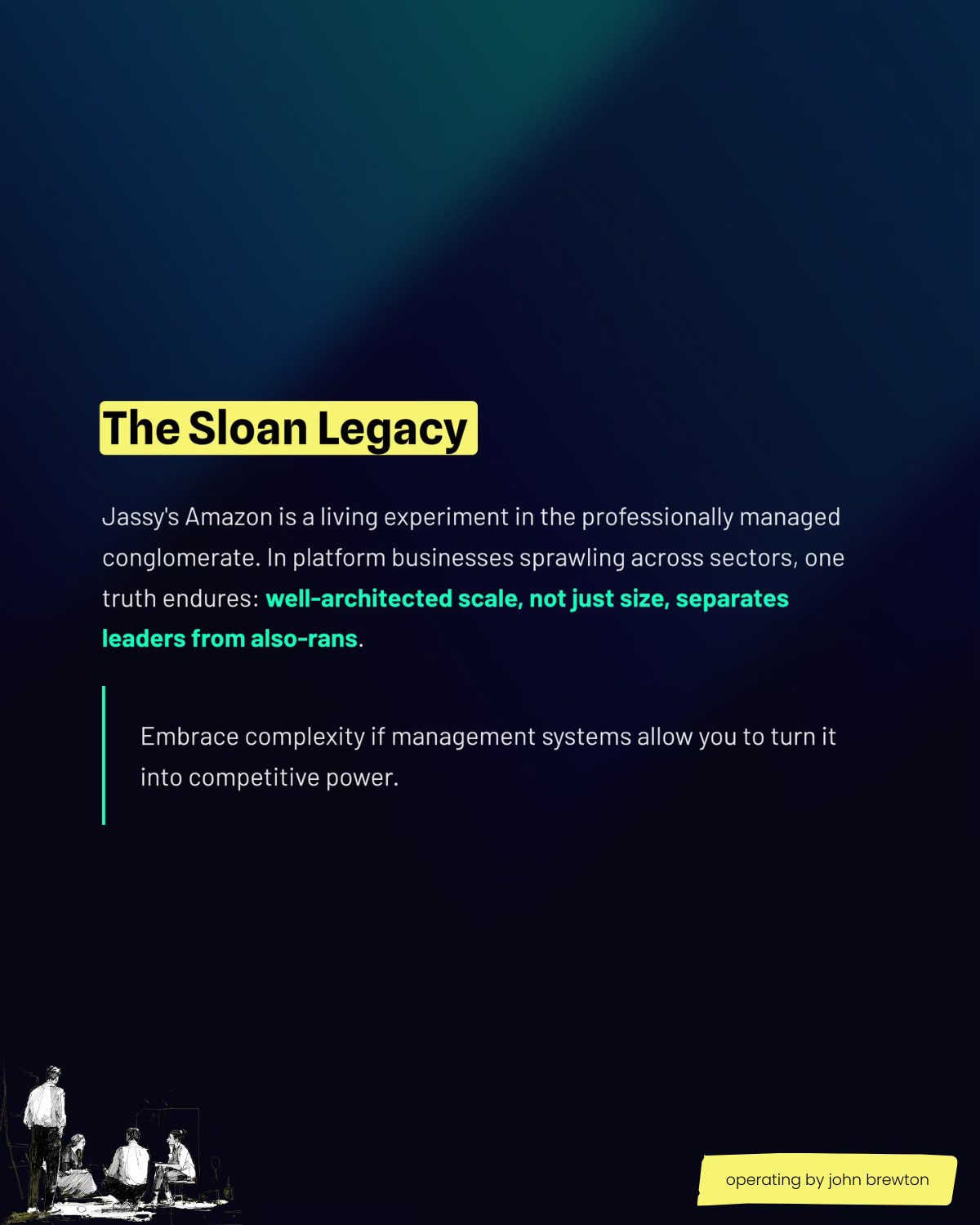

Operating History: Alfred Sloan’s Lessons: Structure for Scale

Link here to exclusive paid subscriber coverage of the Alfred and Amazon relationship.

Four

Deploy capital intensity as a competitive moat. Amazon’s $100 billion+ annual capex is simultaneously a competitive weapon and a barrier to entry. Walmart, Target, and other retailers cannot match this investment level, creating a time-based advantage in automation deployment. By the time competitors respond, Amazon will have accumulated years of learning curve advantages, superior robotics software, and economies of scale in hardware procurement.

This represents an inversion of lean startup orthodoxy. In mature, capital-intensive industries, the optimal strategy may be maximum investment velocity, spending to the edge of capital market tolerance to build irreproducible infrastructure advantages. Amazon’s stock underperformance in 2025 relative to other Magnificent Seven companies (up just 3.9% versus the S&P 500’s 16.5%) suggests the company is testing those limits. But management is explicitly betting that long-term competitive position justifies near-term multiple compression.

The strategic question for competitors becomes: Can they afford not to match Amazon’s capital intensity? If Amazon achieves its automation targets while rivals remain labor-intensive, the cost structure differential could prove insurmountable. This creates a potential arms race dynamic where all major retailers must pursue aggressive automation regardless of financial pressure, simply to avoid being rendered uncompetitive. The industry-wide implications could dwarf Amazon’s individual impact.

The Broader Reckoning

Amazon’s trajectory forces confrontation with a question that has lurked at the edges of economic discourse for decades: What happens when productivity growth and employment growth fully decouple at the firm level?

The post-war economic consensus held that technological progress raised productivity, which increased profits, which funded expansion, which created employment. It was a virtuous cycle where growth and jobs moved together. Amazon and others are engineering the opposite: technological progress that raises productivity, which increases margins, which funds further automation, which explicitly avoids employment. The cycle is still virtuous for shareholders and consumers, but it systematically excludes labor from the value distribution.

The academic literature provides frameworks for understanding this. Acemoglu and Pascual Restrepo’s seminal work on automation identifies two countervailing forces: the displacement effect (technology directly substitutes for labor) and the productivity effect (cost savings enable output expansion that creates new labor demand). The traditional assumption is that productivity effects dominate at the firm level, even if displacement creates negative externalities at the societal level.

Amazon challenges this. Management’s explicit goal is displacement without corresponding productivity-driven job creation. The savings from automation flow to shareholders via buybacks (Amazon recently authorized $20 billion), to consumers via lower prices that defend market share, and to capital reinvestment in more automation.

If this model proliferates, the macroeconomic implications are profound. Amazon remains the second-largest private employer in America. If the top 100 US employers adopted similar labor-intensity reduction targets, and competitive pressure suggests many will, the aggregate employment impact could reach 5-10 million fewer jobs by 2035 under current growth assumptions. Walmart has already committed to flat headcount despite growth. JPMorgan Chase circulated an internal memo emphasizing “a strong bias against hiring,” and Goldman Sachs instructed managers to “constrain headcount growth.”

The question is not whether this is technologically feasible; Amazon is proving that it is, but how it can become socially sustainable. Labor’s share of national income has declined from roughly 65% in the 1970s to under 60% today. If automation accelerates this trend toward 50% or below, the distributional consequences become severe: a shrinking portion of economic output flows to workers, while an expanding share accrues to capital.

Yet constraining automation through policy faces formidable obstacles. Proposals like automation taxes (to capture productivity gains for redistribution), displaced worker funds (requiring companies to finance retraining), or labor board representation (giving workers a voice in automation decisions, as in Germany) all reduce private returns to automation, potentially slowing adoption and making the implementing jurisdiction less competitive globally. This creates race-to-the-bottom dynamics: Amazon can pursue aggressive automation because U.S. corporate governance imposes minimal stakeholder obligations. Jurisdictions that regulate heavily risk losing their corporate tax base.

Operating by John Brewton goes deep on what it takes to build, scale, and optimize modern companies. This Amazon analysis is just the beginning.

What Paid Subscribers Get:

📬 3x Weekly Operating Notes – Short, actionable insights on corporate strategy, operating excellence, and business history

📊 Epic Operating Resource Articles – Deep-dive case studies and frameworks (like the Carnegie, Sloan, and Grove comparisons) available exclusively to paid members

💬 Paid Subs-Only Chat & Operating Working Group – Direct access to John and a community of operators tackling real challenges

🎙️ Quarterly Live Operating Q&A – Community working sessions where we break down current strategies and answer your questions

Operating Founders get even more:

🤝 Quarterly 1:1 Operating Sessions with John – Four 30-minute private sessions per year to work through your specific operating challenges

Plans:

Monthly: $17/month

Annual: $95/year (save 54%)

Operating Founder: $550/year (includes 1:1 sessions)

Most importantly, thank you for reading! I’d love for you to join our growing community and help you solve your biggest operating conundrums in any way I can.

Conclusion: The Optimization Company

Amazon’s evolution over the past two years represents more than quarterly earnings optimization or tactical cost management. It marks a fundamental inflection point in the history of corporate operations, comparable in significance to Alfred Sloan’s divisional structure at General Motors in the 1920s, Toyota’s just-in-time manufacturing in the 1970s, or Dell’s direct-to-consumer supply chain innovation in the 1990s.

What distinguishes Amazon’s current transformation is its systematic application of capital as the primary lever for operational advantage. The company is demonstrating, with remarkable transparency in its financial results, that mature businesses can achieve simultaneous revenue growth and workforce reduction through deliberate substitution of technology for labor. The mathematics are straightforward: $10 billion in robotics investment generating $12.6 billion in labor savings represents a 26% return on a specific class of capital deployment. The strategic insight lies in recognizing that this return exceeds most traditional growth investments while also creating competitive barriers through accumulated learning curves and infrastructure advantages.

The earnings trajectory from Q4 2023 through Q2 2025 provides an unusually clear window into the mechanics of this transition. Operating margins expanding from 7.8% to 11.5% while the company simultaneously invests over $100 billion annually demonstrates that the Bezos-era principle of “long-term thinking over short-term profits” remains intact, just applied to a different objective. Where early Amazon sacrificed profitability to build market dominance, today’s Amazon sacrifices near-term cash flow to build operational dominance through automation and infrastructure density. For an operator like me, it’s a wonder to behold.

This approach represents what might be termed the capital-intensive operations strategy: the recognition that in mature industries with established demand, competitive advantage derives not from discovering new markets but from achieving structural cost positions that rivals cannot replicate. Amazon’s $118 billion in projected 2025 capital expenditure creates a time-based moat, competitors who match this spending three years later will face an Amazon that has already optimized its systems, accumulated operational data, and moved further down the automation learning curve.

The parallel to Amazon Web Services is instructive not just for the J-curve investment pattern, but for what it reveals about strategic sequencing. AWS succeeded because Amazon built expertise in large-scale infrastructure operations for internal use, then commercialized that capability. The current automation strategy follows identical logic: develop sophisticated robotics coordination for warehouses, then potentially license those systems to the thousands of logistics operators who cannot afford comparable R&D investments. The $775 million Kiva Systems acquisition in 2012 appears, in retrospect, as foundational as the decision to build AWS infrastructure that could be externalized.

The business history significance lies in how this strategy could reshape entire sectors. Walmart’s commitment to flat headcount, the logistics industry’s accelerating automation, and corporate services firms deploying AI agents all suggest Amazon is establishing a template rather than an outlier approach. If the efficiency gains materialize as projected, margins reaching 15% by 2028, revenue per employee doubling, the competitive pressure on industry peers to adopt similar strategies becomes overwhelming.

What Amazon will report on October 30th matters less than what the company has already demonstrated: that modern enterprise strategy increasingly centers on the optimization of capital deployment across both digital infrastructure (AWS, AI) and physical operations (robotics, automation) simultaneously. The earnings calls provide a real-time record of management navigating this dual transformation, making mistakes (Q2 2025’s margin miss), adjusting (the 14,000 job cuts to preserve targets), and maintaining strategic conviction despite market skepticism.

For students of corporate strategy and business history, Amazon’s current phase offers a laboratory for understanding how companies evolve when traditional growth constraints (market size, distribution reach) give way to operational constraints (labor availability, capital efficiency). The company is, in effect, answering a question that has lurked in business literature since the first industrial revolution:

What happens when technology enables a firm to grow output while shrinking inputs, and management possesses both the capital and the institutional patience to execute that transformation systematically?

The answer, as revealed through eight quarters of earnings results and internal strategic documents, is that such firms can achieve sustained margin expansion, defend competitive position through capital-intensive moats, and fundamentally alter the economics of their industries. Whether this represents the optimal path for all businesses is sector-dependent. Whether it succeeds for Amazon specifically awaits the completion of this investment cycle around 2027-2028. But that it represents a coherent, historically significant operating strategy is beyond dispute.

Future business historians examining the 2020s will likely identify this period as the moment when capital-labor substitution transitioned from an academic concept or manufacturing-sector reality to a systematic strategy deployed by the world’s largest consumer-facing companies. Amazon’s earnings, read carefully, provide the chronicle of that transition, complete with financial results, management commentary, and market reactions that reveal both the promise and the friction inherent in such profound operational transformation.

For practitioners building and operating companies in the decades ahead, Amazon’s approach offers a beautiful strategic framework: a detailed case study in how patient capital, operational discipline, technological infrastructure investment, and systematic factor substitution can be combined to achieve competitive positioning that may prove difficult to erode. Understanding this strategy, its mechanics, its economics, its sequencing, and its trade-offs becomes essential not because every company should replicate it, but because every operator must comprehend the competitive dynamics it creates.

The lesson, ultimately, is that corporate strategy and operating excellence remain inseparable. Amazon’s financial performance over the past two years demonstrates that the greatest strategic advantages still derive not from clever positioning or marketing innovation, but from superior execution of complex operational transformations that require years of sustained investment and unwavering management focus. That has been true since the days of Carnegie Steel and Ford Motor Company. It remains true in the age of algorithmic operations and artificial intelligence.

The tools change.

The strategic principles endure.

John Brewton writes about business strategy, economic history, and the future of companies at Operating by John Brewton. This analysis draws on Amazon’s public earnings reports, internal documents obtained by investigative journalists, academic research on automation economics, and two years of quarterly earnings calls and analyst reactions.

If you’d like to work together, I’ve carved out some time to work 1:1 each month with a few top-notch Founders and Operators. You can find the details here.

John Brewton documents the history and future of operating companies at Operating by John Brewton. He is a graduate of Harvard University and began his career as a Phd. student in economics at the University of Chicago. After selling his family’s B2B industrial distribution company in 2021, he has been helping business owners, founders and investors optimize their operations ever since. He is the founder of 6A East Partners, a research and advisory firm asking the question: What is the future of companies? He still cringes at his early LinkedIn posts and loves making content each and everyday, despite the protestations of his beloved wife, Fabiola, at times.

How are capital-intensive corporations new? What you are describing sounds to me like a hedge firm, a film production company or a baseball team. Admittedly, not great news for those of us who can't hit a curve ball.

Amazing Amazon (and of course Bezos and Jassy) are laser tuned into successful operating and growth models.