Operating Stories - From Snowboards to $220B: The Tobias Lutke & Shopify Story

What One Frustrated Entrepreneur Can Teach All of Us

In 2026, I’m working directly with 100 creators building real businesses.

I want to bring operating strategy, competitive positioning, and financial planning to a community that’s fundamentally different from my typical industrial and technology clients.

For the first 100 creator founders: Four 60-minute 1:1 advisory sessions for $95.

Context: My standard engagement starts at $10K/month. This isn’t that. This is me learning from you while helping you build something sustainable.

Limited to 100 spots. Message me with questions or to claim yours or just click below to sign up (sign up requires browser access):

Start Here

In 2004, Tobias Lütke wanted to sell snowboards online. He had no credentials, no capital, no connections, and no work authorization in the country where he wanted to start a business. What he did have: two months of uninterrupted time and the ability to code in Ruby on Rails.

By 2006, other entrepreneurs didn’t want his snowboards, they wanted his software. He pivoted. That software became Shopify. Today it powers over 9 million businesses across 175 countries, has facilitated over $1 trillion in commerce, and is valued at approximately $220 billion.

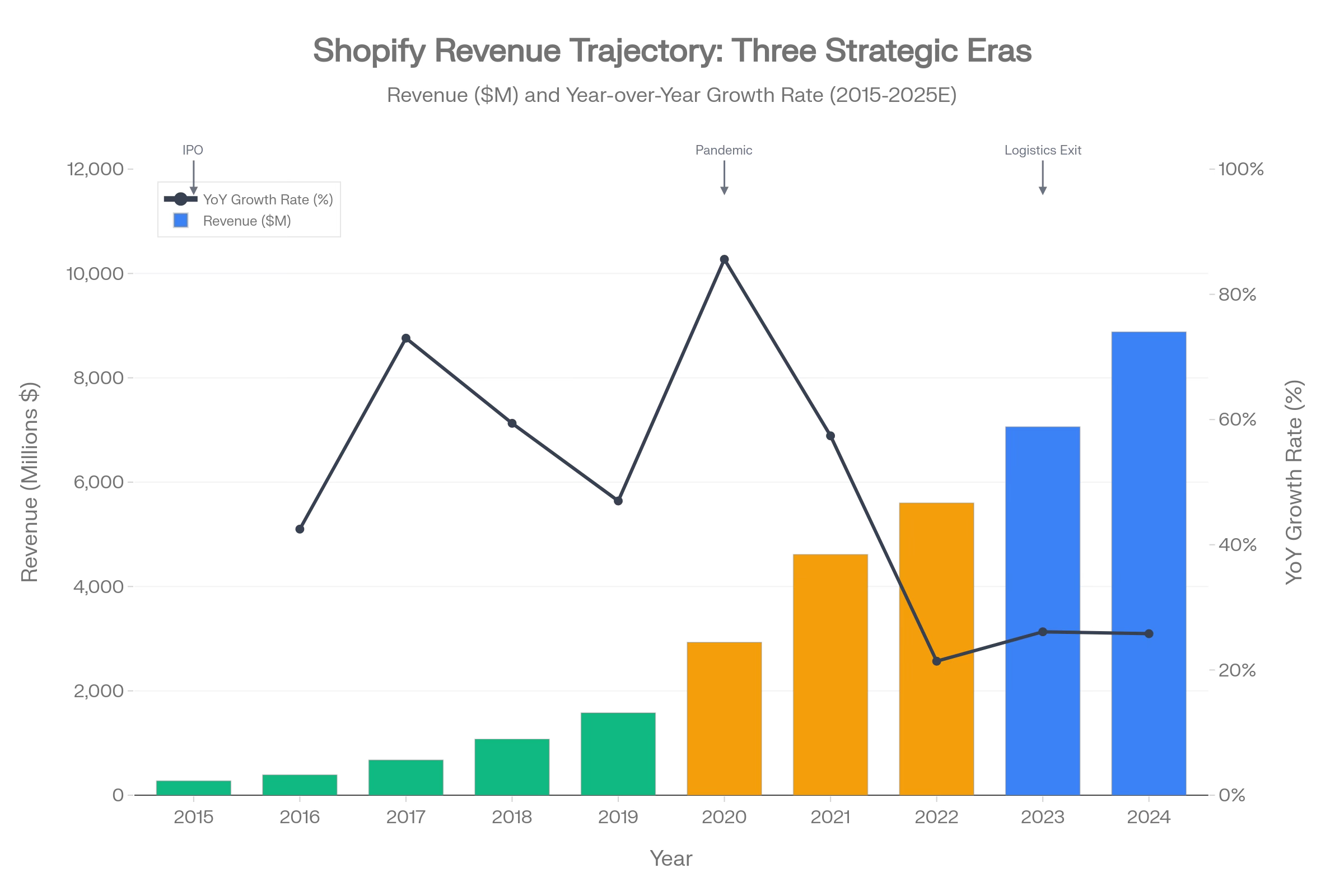

This is not a story about luck or timing. It’s a story about how capital markets force strategic discipline on companies that forget their core competence. Between May 2015 and today, Shopify has filed 42 quarterly earnings reports. Those reports trace three distinct strategic regimes:

2015–2019: Product-led land-grab (clean software story)

2020–2022: Pandemic super-cycle followed by logistics over-reach

2023–2025: Strategic refocus on software and profitable growth

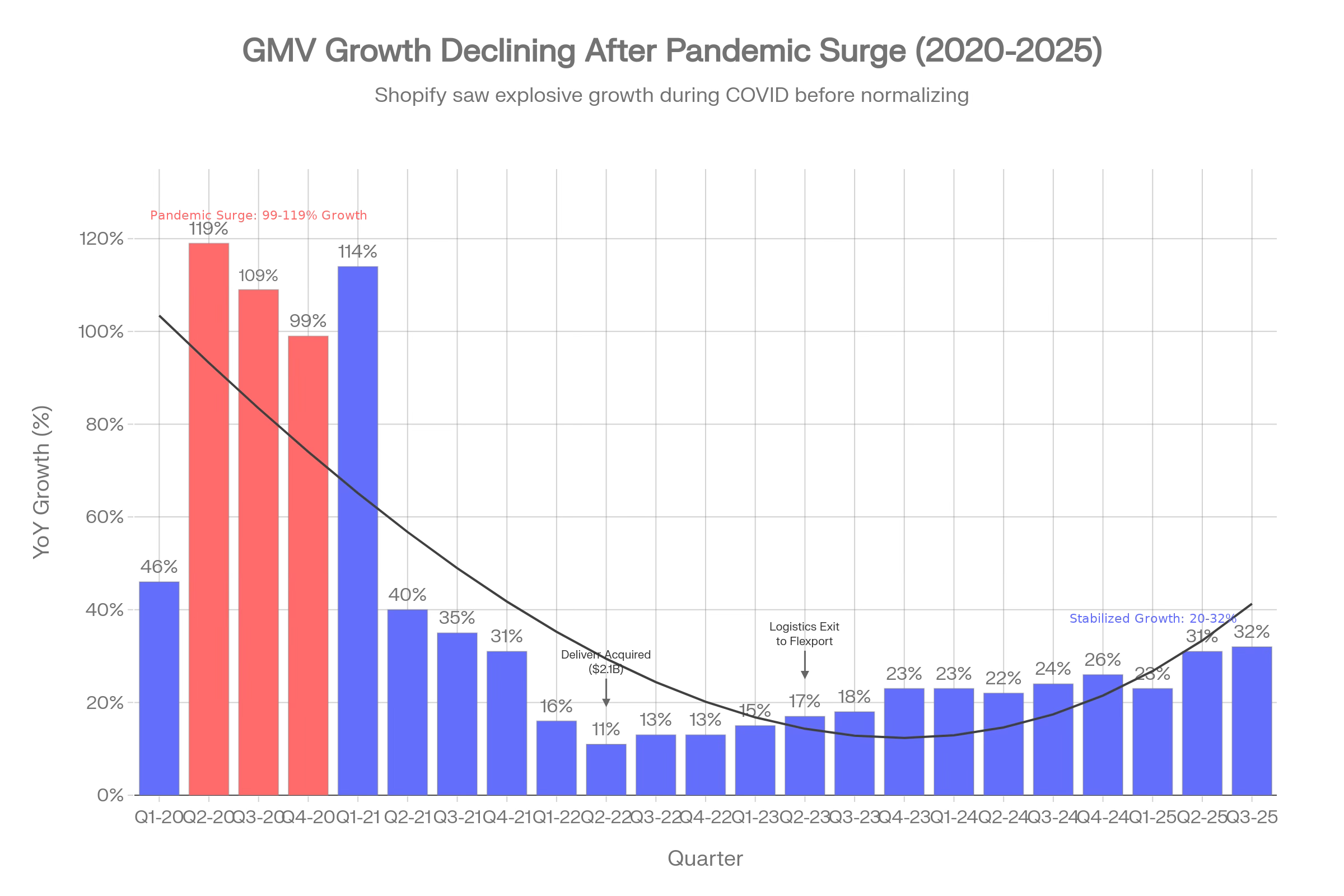

The stock appreciated 4,600% from IPO to May 2020, crashed 70% in 2022, then recovered 200% from its October 2022 low. The company acquired logistics infrastructure for $2.1 billion in May 2022, then sold it less than one year later while laying off 20% of its workforce.

What you’re about to read is not a typical earnings recap. It’s an autopsy of how quarterly communications shape—and are shaped by—public market expectations. And it’s a field manual for operators who need to understand how the companies of the future are built, priced, and disciplined.

Let’s start where Lütke started: with what you already have.

Principle #1: Start With What You Have

Section 1.1: The Capital You Don’t Count

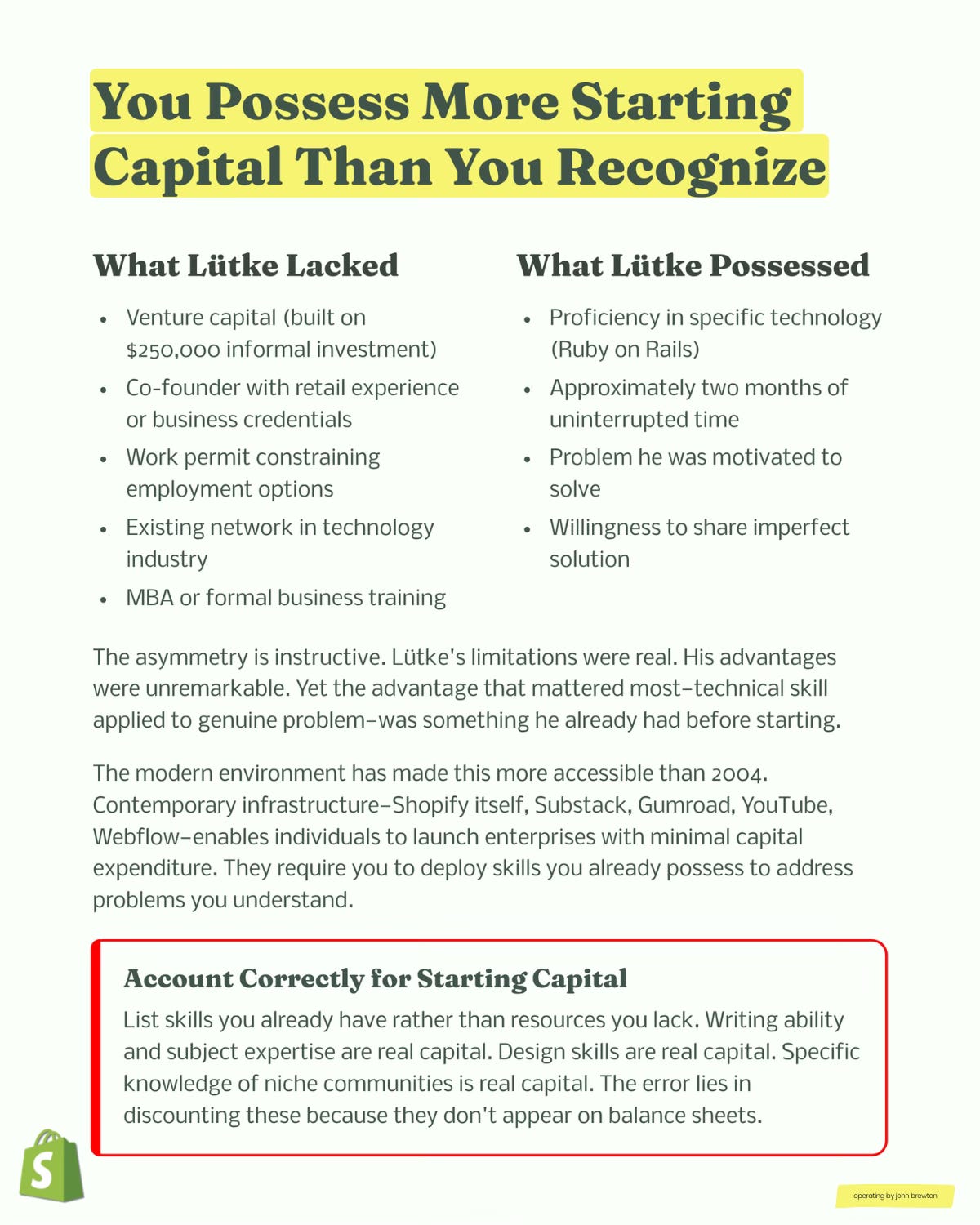

Most people think starting capital means money. Lütke’s story suggests otherwise. When he built Snowdevil (his snowboard shop) in 2004, his balance sheet looked empty by conventional standards. But his capability inventory was rich:

Technical capital: Proficiency in Ruby on Rails at a moment when the framework was nascent

Time capital: Approximately two months of uninterrupted focus

Problem capital: Direct experience with friction that made existing e-commerce platforms unusable for his use case

Distribution capital: Willingness to share an imperfect solution publicly

The asymmetry is instructive. His limitations were real and significant—no venture funding, no co-founder with retail experience, work permit issues constraining employment options, no existing network in the technology industry, no MBA or formal business training.

Yet the advantage that mattered most—technical skill applied to a genuine problem he was motivated to solve—was something he already possessed before deciding to start a company.

Three distinct strategic regimes: hyper-growth (2015-2019), pandemic super-cycle (2020-2022), and disciplined profitable growth (2023-2025)

The chart above shows Shopify’s revenue from IPO through today. Notice three distinct regimes:

Era 1 (2015-2019): Growth rates of 47–95% annually on an expanding base

Era 2 (2020-2022): Pandemic spike (86% growth in 2020), then deceleration to 21% in 2022

Era 3 (2023-2025): Stabilized at 24–26% growth with dramatically improved profitability

Operating Takeaway: Redefine Your Starting Capital

Most operators systematically undercount their starting capital. They inventory what they lack (funding, network, credentials) and ignore what they possess (domain expertise, technical skills, time, specific knowledge of a friction point).

A more useful framework:

List skills you already have rather than resources you lack

Writing ability and subject expertise are real capital

Design skills are real capital

Specific knowledge of niche communities is real capital

Time you control is real capital

The error lies in discounting these because they don’t appear on balance sheets. But Lütke’s story, and the 4,600% stock appreciation that followed, demonstrates that the most durable competitive advantages often come from deploying existing capabilities against problems you understand deeply.

The modern environment amplifies this advantage. In 2004, Lütke needed to build infrastructure from scratch. Today, platforms that didn’t exist then—Shopify itself, Substack, Gumroad, YouTube, Webflow—provide scaffolding for enterprises. Financial barriers to starting have declined. Ability to reach customers directly has improved. Cost of learning new skills has fallen.

The question isn’t whether you possess sufficient advantages. The question is whether you’re willing to start with what you have.

Principle #2: Listen to Markets

Section 1.2: The Pivot That Markets Demanded

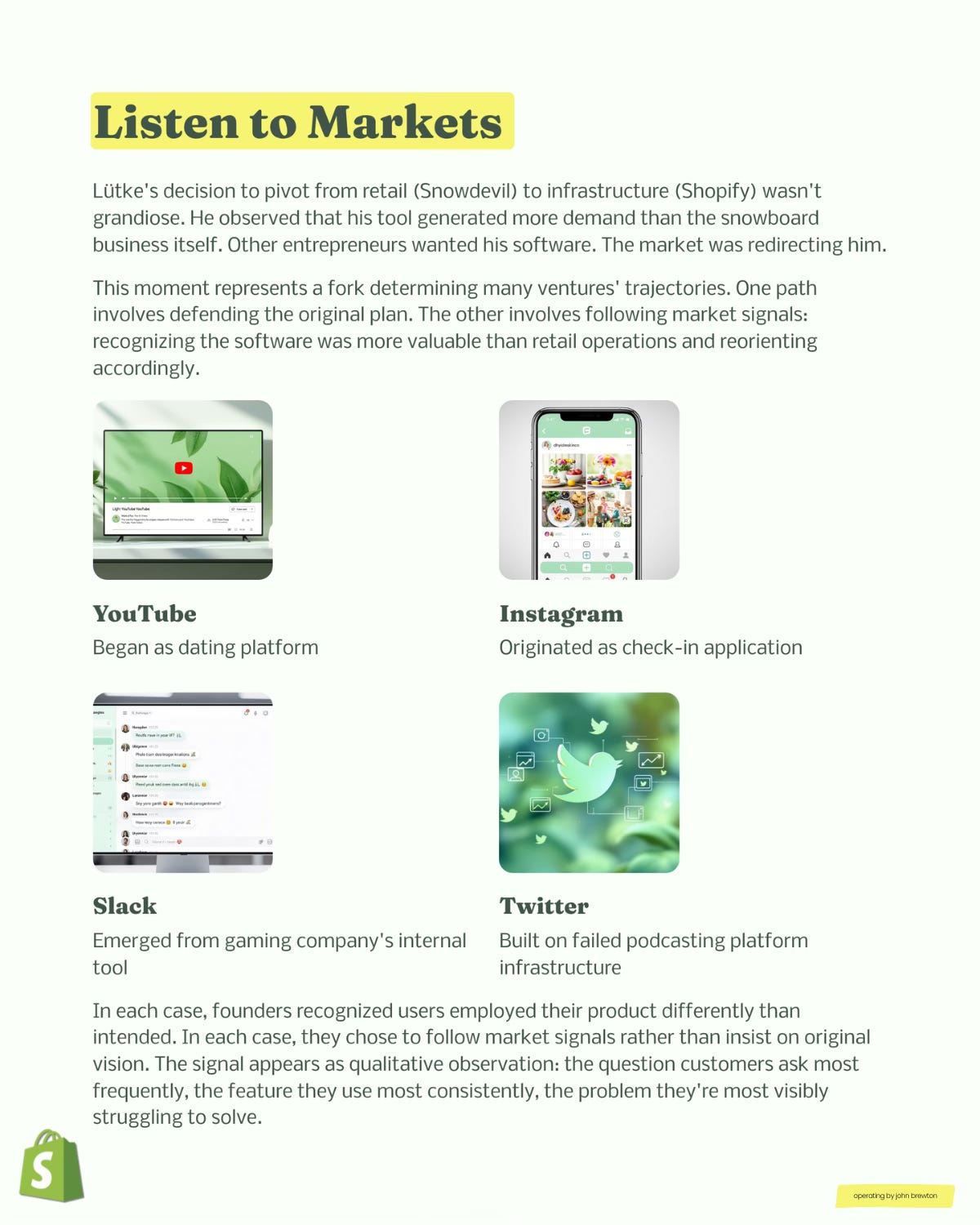

Lütke’s decision to pivot from retail (Snowdevil) to infrastructure (Shopify) in 2006 wasn’t about visionary foresight, it was about pattern recognition. I think it was about humility. He observed that his tool generated more demand than the snowboard business itself. Other entrepreneurs wanted his software. The market was redirecting him.

This moment represents a fork that determines many ventures’ trajectories. One path involves defending the original plan, insisting that retail was the “real” business and software was merely supporting infrastructure. The other path involves following market signals: recognizing the software was more valuable than retail operations and reorienting accordingly.

The market speaks through price, but also through less obvious signals. For Shopify in 2006, those signals appeared as qualitative observations:

The question customers asked most frequently (not about snowboards, but about the software)

The feature they used most consistently (the platform, not the product catalog)

The problem they were most visibly struggling to solve (building online stores)

Similar examples appear across successful pivots:

YouTube began as a dating platform; users uploaded non-dating videos

→ pivoted to general video hosting

Instagram originated as a check-in application (Burbn); users primarily shared photos

→ stripped to photo-sharing only

Slack emerged from a gaming company’s internal tool; outside teams wanted to use it

→ spun out as standalone product

Twitter was built on failed podcasting platform infrastructure (Odeo); short-status updates were the breakout feature

→ became the core product

Operating Takeaway: Treat Demand Curves as Information Events

When market signals diverge from your original plan, that’s an information event—not a distraction. The instinct to defend the original vision is strong, especially when you’ve invested time explaining it to others. But markets reveal preferences through behavior, not stated intentions.

Your job as an operator is to remain attentive to:

Usage patterns that differ from design intent: If customers use your product for an unintended purpose more frequently than the intended one, you’ve discovered a new problem to solve

Questions that cluster around unexpected features: The question customers ask most often reveals their primary friction point

Willingness to pay for byproducts: If a component you considered secondary generates more commercial interest than your core offering, the market is sending a signal about value

The companies that scale are often those that recognized these signals early and pivoted before capital constraints forced the issue. Lütke could have insisted that Snowdevil was the “real” business. Instead, he followed the signal. By Q4 2015 (first full quarter post-IPO), Shopify was already processing $2.8 billion in GMV and growing revenue at 99% year-over-year.

The market told him what it wanted. He listened.

Principle #3: Solve the Problem You Actually Experience"

Section 2.1: When Pull-Forward Demand Looks Like Permanent TAM Expansion

Between Q2 2020 and Q4 2021, Shopify experienced the most dramatic demand acceleration in its history. Q2 2020 revenue grew 97% year-over-year. GMV surged 119%. New stores created jumped 71% quarter-over-quarter. The stock reached an all-time high of approximately $350 (split-adjusted) in November 2021.

Management called it a “once in a generation” demand shift. Offline merchants, forced online by pandemic lockdowns, scrambled to build digital storefronts. Shopify was the obvious choice. The company introduced a 90-day free trial (March 21 – May 31, 2020) to capture the merchant influx, and merchants replaced 94% of lost point-of-sale GMV with online sales.

The pandemic pull-forward is unmistakable: from 119% growth in Q2 2020 to just 11% by Q2 2022